2022 Gold Mid-Year Outlook

The second half of 2022 will be challenging for investors, needing to navigate rising interest rates, soaring inflation, and resurfacing geopolitical issues. The speed at which central banks around the world tighten monetary policy in an effort to control inflation, will probably continue to influence how responsive gold is to real rates in the near term.

Rate hikes could create headwinds for gold, but many hawkish policy predictions have already been factored in. In addition, ongoing inflation and geopolitical risks will probably sustain demand for gold as a hedge. Gold may benefit from underperformance of stocks and bonds in a potential stagflationary environment.

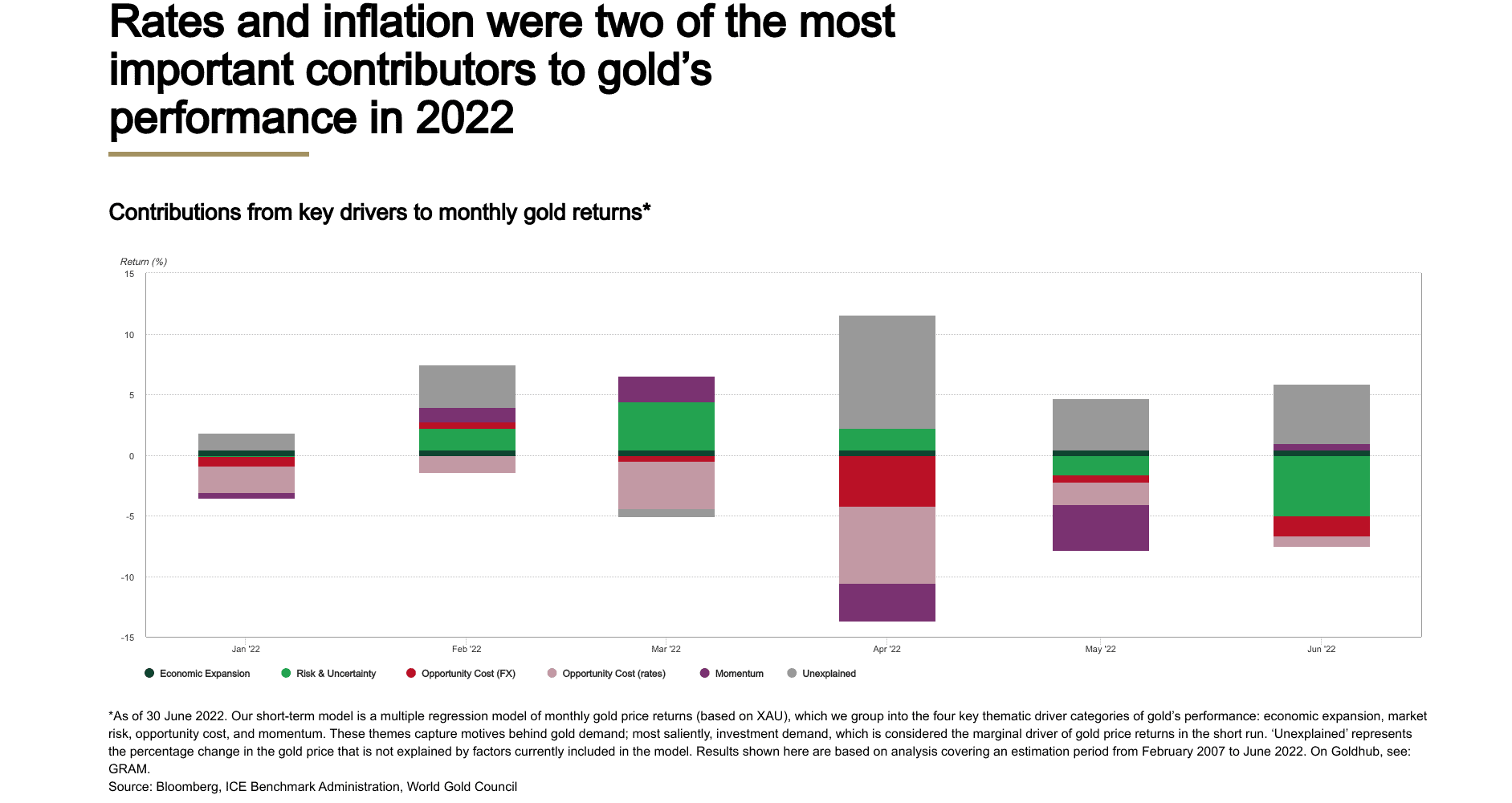

Higher rates in 2022 outweighed inflation risks

Gold increased 0.6% to close at US$1,817/oz in the first half. As the Ukraine conflict developed and investors sought high-quality, liquid hedges amid rising geopolitical uncertainty, the price of gold initially climbed. But as investors’ focus shifted to monetary policy and increased bond yields, gold lost some of those early gains. Due to the struggle between an environment of high risk and rising interest rates, the price of gold had stabilized by mid-May. The latter was a result of a combination of factors, including persistently high inflation and possibly support from the extended conflict in Ukraine and its potential knock-off effects on global growth. Earlier in the year, the latter witnessed significant investment before reversing some of its gains in May and June. However, year-to-date inflows into gold ETFs reached US$15.3 billion (242 tonnes) at the end of June.

Rising opportunity costs, caused by higher rates and a stronger dollar, were a major headwind to gold’s performance year to date, but rising risks, brought on by inflation and geopolitics, drove gold higher for much of the period.

Notably, while the strengthening of the US dollar against a wide range of currencies has hampered the price of gold (when expressed in US dollars), at the same time it has supported the performance of gold in many other currencies, including the euro, yen, and pound sterling, among others.

Additionally, gold was one of the top performing assets during H1, despite its flat year-to-date performance initially appearing uninteresting. It not only generated positive returns, but it also did it with volatility that was below average. As a result, during this volatile period, gold has actively assisted investors in limiting losses. Especially in light of the fact that both equities and bonds, which typically make up the majority of investors’ portfolios, showed negative returns.

Investors’ behaviour in the second half of 2022

During the second half of the year, it is expected that investors continue to face significant challenges. As a result, they will have to balance a number of competing risks compounded by some degree of uncertainty about their magnitude.

Although the majority of central banks were expected to raise policy rates this year, many have taken more aggressive action in response to persistently high inflation. The Bank of England has raised its base rate five times since November 2021, to 1.25%, the Swiss National Bank raised rates for the first time in 15 years, the Fed hiked its funding rate by 1.5% so far this year, the Royal Bank of India is expected to significantly raise its repo rate before the end of the year among developing economies.

The financial markets, including gold market, have been significantly impacted by these actions. The performance of the gold price has historically been influenced by investor expectations of future monetary policy decisions, according to data. Furthermore, historical research shows that gold has underperformed in the months preceding a Fed tightening cycle, only to considerably outperform in the months following the first-rate hike. In contrast, US equities performed best just before a tightening cycle began, but then delivered softer returns.

Main factors affecting Gold’s behaviour

Two major challenges for gold in the second half of 2022 are higher nominal interest rates and a potentially stronger dollar. However, other, more supportive factors may balance out the negative effect from these two drivers. Such as:

- persistently high inflation, with gold playing catch-up to other commodities,

- market turbulence brought on by changes in monetary policy and geopolitics,

- the need for effective hedges that overcome potentially higher correlations between equities and bonds.

In this situation, gold will probably continue to play a strategic and tactical role for investors, especially as long as uncertainty is high.