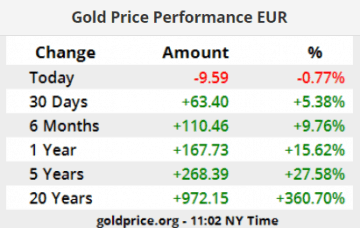

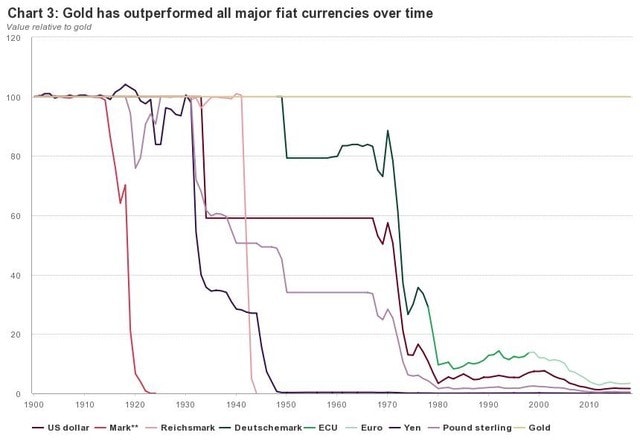

A Paradigm Shift to Gold in 2019

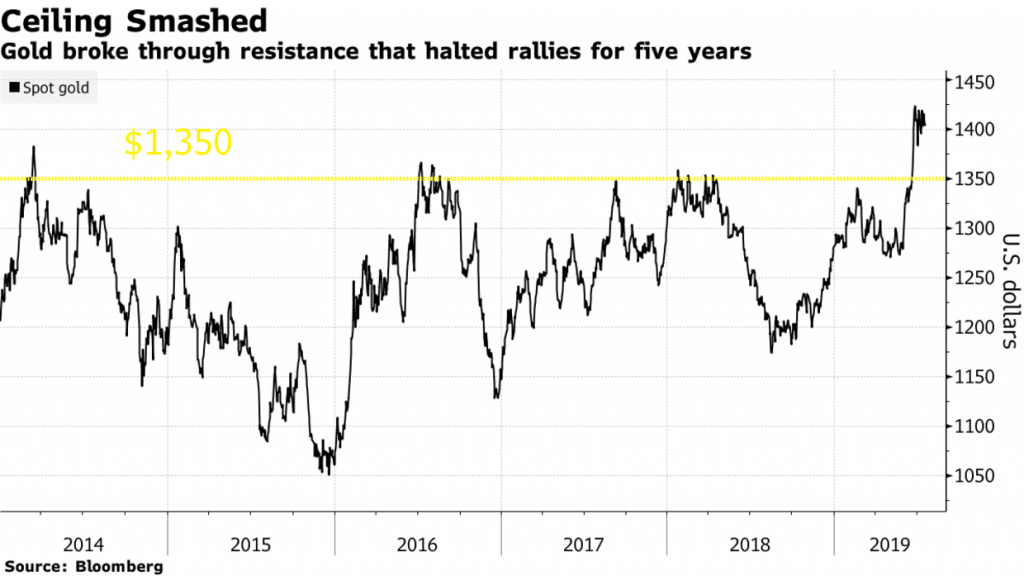

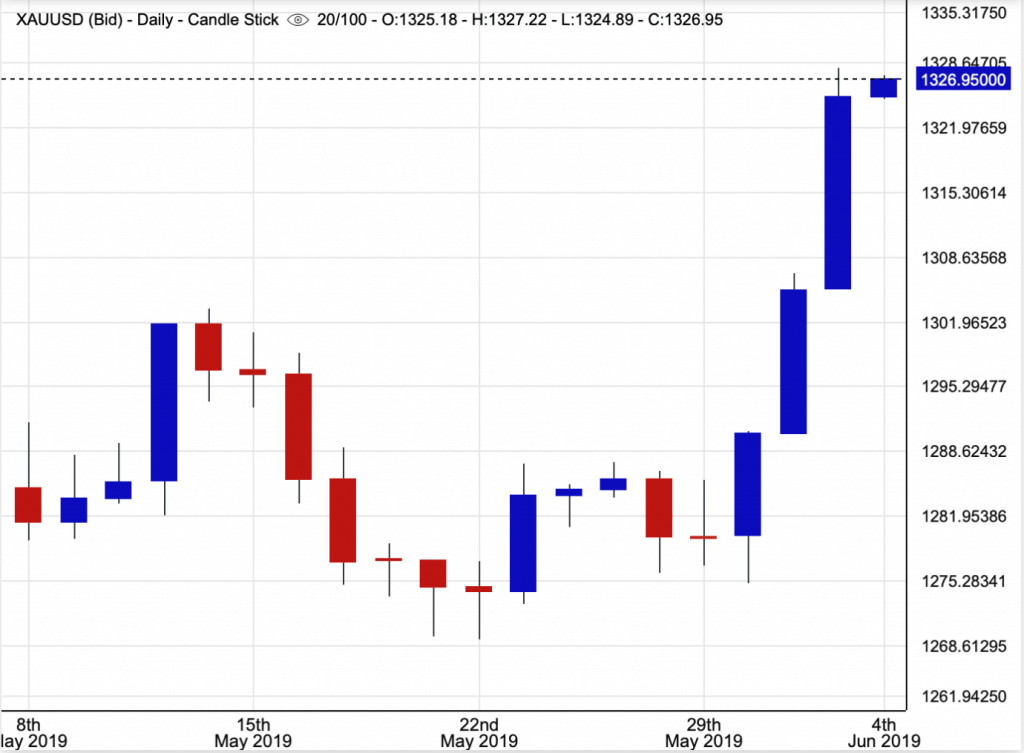

In June, gold finally broke through the technical US$ 1.360 barrier and has been moving steadily around the US$ 1.400 level since, reaching its highest level at US$ 1.453,09 on 19thJuly, since May 2013. The headlines are signaling a gold bull market developing from news reporters, to banks and central banks, to gold miners. Naturally, there are always reasons why a certain asset class develops in any specific way. For gold at the current moment there are at least 6 strong catalysts that are all converging at the same time which are analyzed here under.

1. Basel III – 0% Realization Risk Weight on Gold

Basel III went into effect worldwide on 1stApril, 2019. Non-liquid assets are evaluated in the bank statements of banks under the consideration of the difficulty to liquidize an asset. The specific difficulty to liquidize a non-liquid asset is entered in the books in form of a value deduction. The value deduction may be a few percent (10,20,25%) depending on the asset. For gold the BIS decided that the banks are allowed to enter physical gold held without any value deduction and thus gold is now considered in balance sheets as 100% equal to cash on account, i.e. a 0% realization risk weight. This is applicable for gold with a minimum purity of 995.0, i.e. fine gold.

This signifies a reversal in attitude and policy and giving a gold an official recognition in the international financial system; a step towards re-monetarization of gold. It is also a reason why there is no VAT on fine gold in the EU.

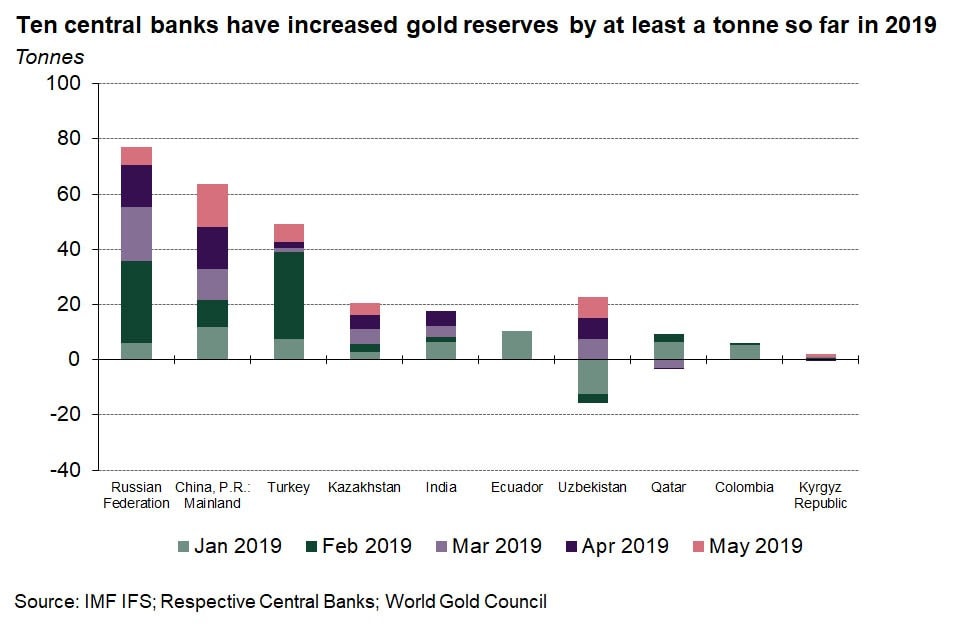

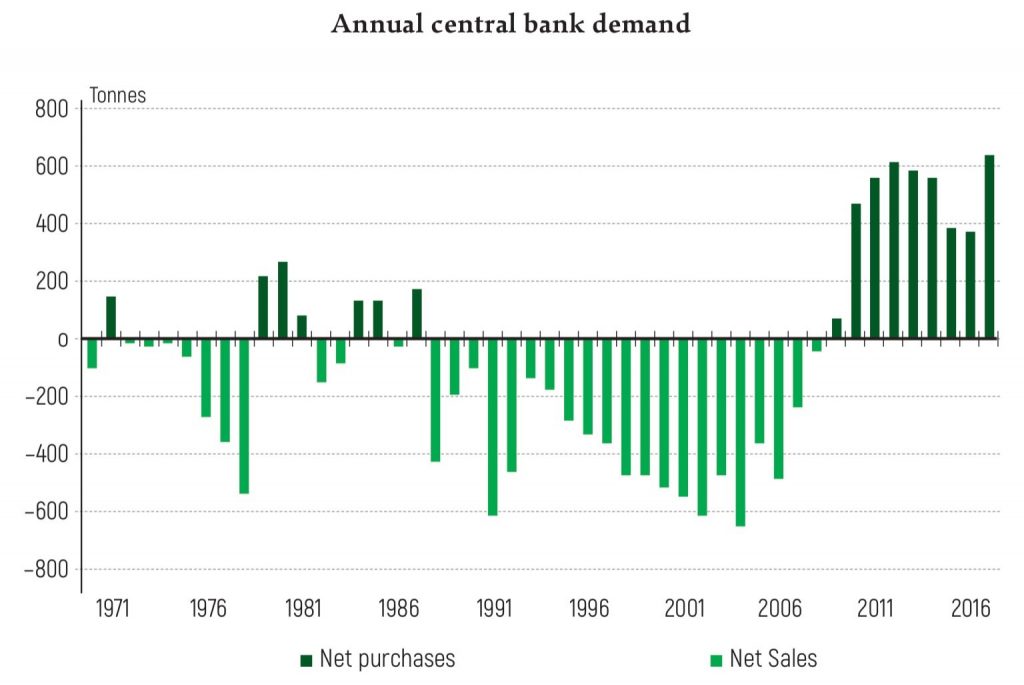

2. Central Banks are on a Gold-Buying-Spree

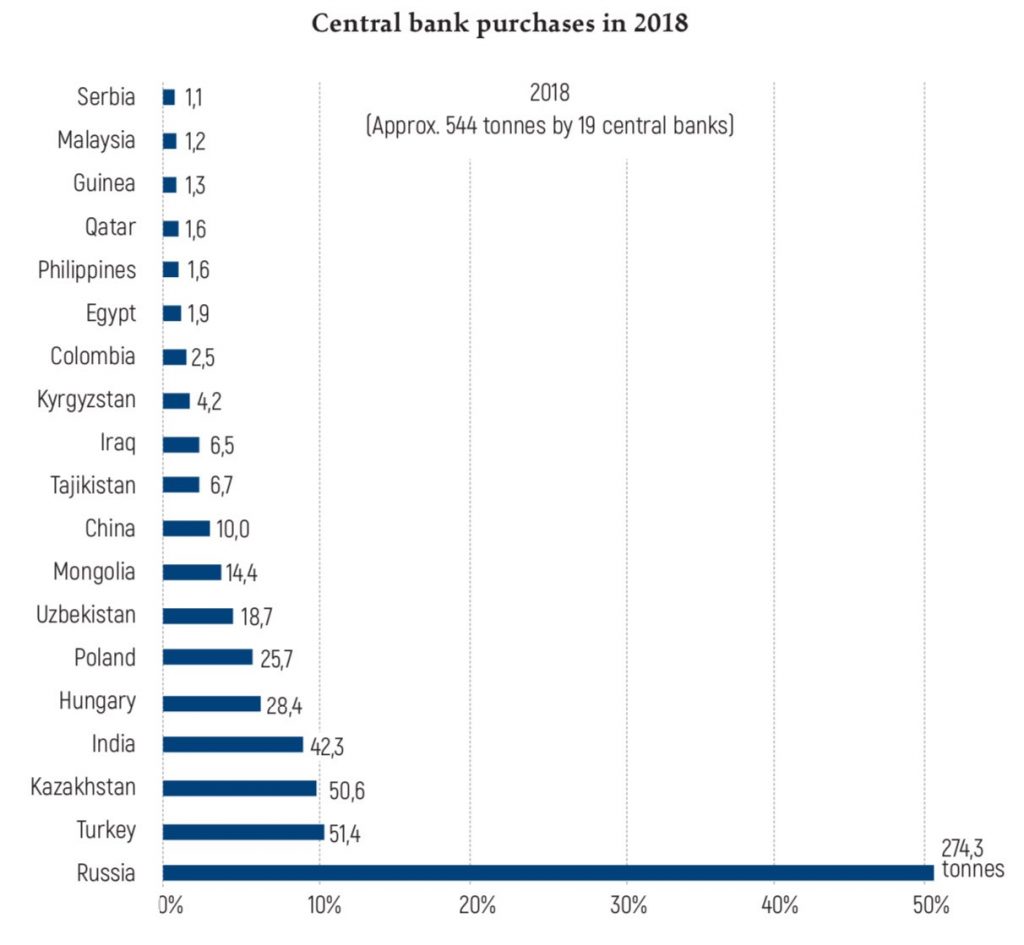

For the first time in generations, central banks are treating gold like money. In 2010, we saw a reversal in the attitude of Central banks that changed from being net sellers of gold to net buyers. Since then this trend has been ongoing, peaking in 2018 in which Central Banks bought a record amount of 651 tonnes of gold. The highest level since 1971 following the Nixon era, when the USD was de-linked from the Gold Standard. 2018 also marked a 75% increase on 2017.

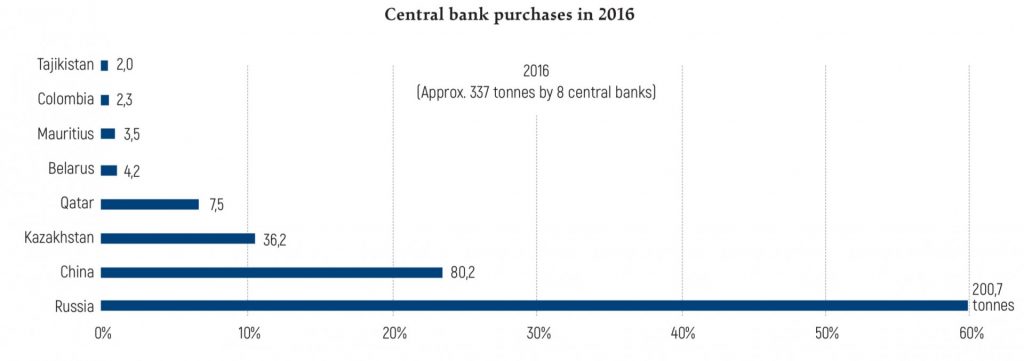

Russia – the Top Net Buyer

Russia has become the 5thlargest net holder of gold. In 2018 Russia got rid of nearly US$ 100 billion of US Treasuries and according to the World Gold Council replaced much of this with gold.

A major reason for this is to reduce its dependence on the US Dollar by using gold as money.

In 2016, for example, Turkey and Iran were engaged in a “gas for gold” plan. With Iran under US Sanctions through this plan Turkey could import gas from Iran and pay in gold.

Gold will aid in conducting business and settling trade independent of the US Government in the near future.

3. China’s Golden Alternative

With the growing tensions in North Korea in 2017, the US threatened to kick China out of the US dollar system if it didn’t coerce on North Korea. This would have left China struggling to import oil and engage in international trade bringing its economy to a halt.

In order for this not to happen, last year the Shanghai International Energy Exchange launched a crude oil futures contract denominated in Chinese Yuan. This would be the first time that large oil transactions are allowed to be made outside the US dollar system since World War II.

Large reserves of Yuan are however also a problem which most oil producers do not wish to maintain. As such, China has linked the crude futures contract with the ability to convert the yuan into physical gold, without touching the Chinese government’s official reserves, through gold exchanges in Shanghai and Hong Kong.

This will allow gold producers to sell oil for gold completely bypassing any restrictions, regulations or sanctions of the US financial system. Additionally, a lot of money will flow into yuan and gold as opposed to us dollars and treasuries.

Doing the math:

China is the world’s largest importer of oil.

To date, China has imported an average of 9.8 million barrels of oil per day which is expected to grow at least 1% per year.

With the oil price currently hovering at US$ 60 per barrel, China is spending around US$ 588 million per day on oil import.

Current gold price is US$ 1.411 an ounce, and thus this equates to an oil import worth over 416.726 ounces of gold per day.

Looking at this from a conservative aspect and assuming only half of the Chinese oil imports will be purchased in gold soon, this would translate into an increased demand of more than 80 million ounces per year, or more than 70% of gold’s annual production.

This increased demand will doubtlessly shock the gold market when and if this shift takes place and this is a big step towards gold’s re-monetarization.

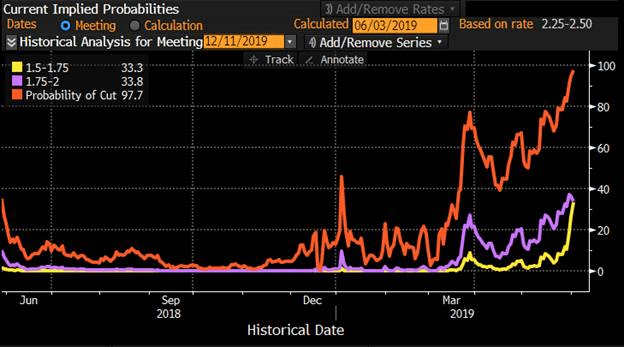

4. The FED

Following the 2008 crash, the Federal Reserve implemented several emergency measures which were promised to be temporary at the time. Through Quantitative Easing (QE), i.e. money-printing, the Fed created US$ 3.7 trillion out of nothing which was used to buy mainly government bonds bloating the Fed’s balance sheet. The Fed also brought the interest levels down artificially to 0% which is the lowest in US history, and kept them there for the following 6 years.

In 2016 the Fed began its attempt to normalize its monetary policy by a. raising interest rates and b. reducing the size of its balance sheet to more “normal” levels. Interest rates rose from 0% to 2.5% and the Fed drained over US$ 500 billion from its balance sheet (11% from its peak).

The S&P 500 eventually peaked in September 2018 only to crash 19% by late December marking the worst December in stock market history since December 1931 during the Great Depression.

This spooked the Fed and instead of normalizing its monetary policy it announced that it would not raise interest rates in 2019 earlier this year. The Fed further announced it would phase out its balance sheet reduction program in Autumn.

This just shows how dependent the US economy is on artificially low interest rates and easy money and it is impossible for the US government to normalize interest rates with an abnormal amount of debt.

Following the nearly 6 years of 0% interest rates it has shown how the US economy is hooked on “easy money” and that it cannot even tolerate a modest decrease in the Fed’s balance sheet and a 2.5% interest rate which is still far below historical averages.

It seems the monetary tightening cycle is over and the next move is a return to QE and 0%, or even negative, interest rates. This would weaken the dollar but would no doubt be good for gold.

With the Feds move from tightening to signaling future easing, the Fed has turned a major headwind for the gold market into a tailwind.

5. Mergers & Acquisitions in the Gold Mining Industry

We have seen a number of mega deals since beginning of 2019 which is a signal that the largest gold mining companies believe gold and gold stocks are currently cheap with a positive increase on the horizon. It shows that the preference is yet to buying out other companies to grow rather than discovering and developing new resources. A major tailwind for gold and 2019 may well go down as a record-breaking year for gold M&As should this trend continue.

Some notable M&As this year:

- Newmont Mining completed a $10 billion takeover of Goldcorp on April 18.

- Barrick Gold acquired Randgold Resources in a $6 billion transaction that closed on January 1.

- Barrick Gold has also announced a joint venture with Newmont after a hostile bid from Barrick failed. Barrick and Newmont, being the top two gold-producing companies in the world, will create the largest gold-producing operation in the world.

6. Gold-Backed Cryptocurrencies

Peter Grosskopf, the CEO of Sprott, recently called gold-backed cryptocurrencies “the most important thing to happen to the gold market in the last several decades.”

Gold-backed cryptos are currently shooting out of the ground as they combine the best of both allowing anyone anywhere in the world to send small or large amounts of gold reliably and without interference, even just with a tap on your smart phone. They are revolutionizing the monetary system and making the use of gold as money ever more convenient for the average person or business.

In a Nutshell we have the Following Big Picture:

- Basel III puts gold into the money category again.

- Record amounts of gold are being bought by Central Banks.

- US sanctions have pushed countries to using gold in a creative manner.

- The Fed’s reversal has worked well for the strength of gold against the dollar.

- The increased number of M&As in the gold mining industry is a bullish sign for the gold price.

- Gold-back cryptos are making the use of gold easier than ever.

Either of these catalysts would have a positive development on the gold price. With all the above converging at the same time, we could well be looking at a strong bull market.

Industry Experts Predict:

Mark Mobius says that gold’s set to push higher, potentially topping US$ 1.500 an ounce. He also added that [physical] gold should always form part of a portfolio, with a holding of at least 10%.

Paul Tudor Jones states: “If it hits $1,400, it will quickly move to $1,700, he said.”

Gold prices are set to “reach $2,000 by the end of the year,” predicts David Roche, president and global strategist at London-based Independent Strategy.

Credit Suisse and Morgan Stanley see gold having strong gains in the second half of 2019. Credit Suisse analysts see gold returning to its record nominal high of US$ 1.921 an ounce:

“Bigger picture though, given the magnitude of the base, which has taken six years to form, we suspect we could even see a retest of the $1,921 record high,” according to David Sneddon, global head of technical analysis at Credit Suisse.

Gold has established a multiyear base that could provide the platform for a “significant and long-lasting rally” for gold, he said. We concur with this view and indeed are more bullish as we see gold going to well over $3,000/oz in the long term.

Why LIEMETA ME Ltd?

LIEMETA ME Ltd, Nicosia, Cyprus, provides physical storage of precious metals at its prime location in Liechtenstein as well as trade services of precious metals, mainly gold, silver, platinum and palladium.

Your precious metals are safely and securely stored “segregated and allocated” and we are one of the few physical storage houses for precious metals that provide full-cover insurance, including embezzlement.

Stored assets are fully legally owned by the client, client assets are of course not on our companies’ balance sheets.

LIEMETA is a privately owned, independent and non-bank company, meaning that its services do not fall within the scope of CRS or AEOI.

LIEMETA provides 100% discretion, 24/7 access to clients’ stored assets at its sophisticated unit and high-security building.

LIEMETA is proud to be chosen by high net-worth individuals as their trustworthy custodian, in Liechtenstein.

You are welcome to contact us through the below contact form.

We do not offer investment advice:

This information is provided solely for general information and educational purposes. It is not, and should not be construed as, an offer to buy or sell, or as a solicitation of an offer to buy or sell.

Amanie Supervisors’ Shariah Supervisory Board during its meeting, presided by Scholar Dr Mohamed Ali Elgari, evaluating the Shariah compliance of Liemeta’s gold and silver sales and storage procedures, September 2019.

Amanie Supervisors’ Shariah Supervisory Board during its meeting, presided by Scholar Dr Mohamed Ali Elgari, evaluating the Shariah compliance of Liemeta’s gold and silver sales and storage procedures, September 2019.

Recent Comments