Cyprus: Cash in Deposit Boxes – What will happen later?

As per the Financial Mirror, Bank of Cyprus and Hellenic Bank have leased 17.000 security deposit boxes. Is this really a safe option? Is hoarding cash balances with banks abroad a safe option? Or would physical gold bars stored outside the banking system be safer?

During the crises in Cyprus in 2013, overnight people lost savings above a €100,000 as the casino bankers at Laiki Bank went under and Bank of Cyprus had to recapitalize itself. Unsurprisingly, trust issues in the banks remain front and centre to this day, the Financial Mirror wrote.

Lack of trust in Cyprus Banks

The lack of trust in Cyprus Banks directed many bank customers to alternative solutions, and that’s why people of Cyprus store cash money, gold bars, jewellery and other valuables in 17.000 deposit boxes at banks. Others opened bank accounts in the UK and other countries and sent funds out there.

After the crises in 2013, the government considered to confiscate the contents of all deposit boxes at banks. This intention created a huge public protest and consequently, the government dropped its intention.

Bank of Cyprus (BoC) chairman Josef Ackermann said on the Limassol Economic Forum last year in October that “banks are better regulated now, they have come a long way, but they are not safe enough.”

Banks and officials don’t get tired of repeating that more than 50% of all bank accounts in Cyprus are under the cover of the “Deposit Guarantee and Resolution of Credit and Other Institutions Scheme”, insuring bank account balances up to €100.000. That’s right as far as the coverage is concerned. But the Cyprus Deposit Guarantee Fund for Banks, which is the source for those compensation payments in case of defaulting banks, has only less than €80 million funds available, which is nothing even in case of a small bank defaulting.

Non-performing loans, shortly NPLs, remain as a serious risk in the banking sector, although banks were able to lower their NPL exposure by selling off some of their NPLs to buyers of distressed loans.

How safe are deposit boxes with banks?

The majority of deposit is not aware of these two facts:

- Content of deposit boxes is considered bank property in case of a bank’s bankruptcy

When a bank goes bankrupt, everything within a bank belongs to the bank and becomes a part of the bank’s assets, unless the owner of belongings proofs to the liquidator that not the bank is the owner of a specific belonging but s/he her/himself.

The pure fact that one is the lessee of a deposit box in a bank does not necessarily mean that s/he is the owner of its content. The legal ownership must be proven with documents.

Hard days to come for those who can’t, for whatever reasons. - Reporting of deposit boxes with banks

As per the current 5th EU AML Directive (Directive on the prevention of the use of the financial system for the purposes of money laundering or terrorist financing), “the identity of holders of bank or payment accounts and safe-deposit boxes, their proxy holders, and the beneficial owners is ensured.” Furthermore, EU member states are required to “establish centralised automated mechanisms, e.g. a register or data retrieval system, (to ensure) timely access to information (mentioned above).

As beneficial ownership of safe-deposit boxes can only be related to the content of boxes, and not the boxes itself, which are property of the banks, banks are expected to apply due diligence and compliance procedures to the content of deposit boxes.

As per the current 5th EU AML Directive (Directive on the prevention of the use of the financial system for the purposes of money laundering or terrorist financing), “the identity of holders of bank or payment accounts and safe-deposit boxes, their proxy holders, and the beneficial owners is ensured.” Furthermore, EU member states are required to “establish centralised automated mechanisms, e.g. a register or data retrieval system, (to ensure) timely access to information (mentioned above).

As beneficial ownership of safe-deposit boxes can only be related to the content of boxes, and not the boxes itself, which are property of the banks, banks are expected to apply due diligence and compliance procedures to the content of deposit boxes.

The application of this obligation will surely delay a bit in Cyprus, as usually, and it remains to be seen how banks will be handling this.

Undeclared content of deposit boxes will probably create headache when this information arrives the tax authorities.

Cash on current account creates losses

Holding cash balances on bank current accounts, be it in Cyprus or abroad, is generally the surest way to lose money. However, this is the most common way that people keep their money.

With an EU-wide average Euro inflation rate of 1,71% annually during the period 1999 – 2019, €100.000 on a bank account in 1999 has a purchase power of only €70.825 in 2019, a loss of more than 30%.

This could be compensated with time deposits (fixed deposits) granting an interest income. To safe the same purchase power of €100.000 from 1999 to 2019, a bank customer needed an average annual interest rate of 1,7396%, based on the EU average figures.

However, banks currently offer 0 to 0,3% interest of fixed deposits.

And: Keeping little or bigger wealth on bank accounts only, does not shield money from risks of the banking sector in general and from the risk of bank defaults (bankruptcy), as ex-customers of Laiki Bank know well. It does also not protect against defaulting countries and later possible hair-cuts, like it happened in Greece, unfortunately.

Physical gold as an alternative

Ideally, wealth should be diversified and invested into different asset classes. Everybody knows the famous word, “don’t put all eggs in one basket”.

Many people invest in real estate property, which is not a bad idea in general. However, the big downturn of property is the fact that it is not a liquid asset and a property owner may need months or even years to sell the property when s/he needs money.

Government bonds may be risky, depending on the issuing country, or provide only a very small yield, or even a negative yield, as it is the case with German government bonds. American T-Bonds (Treasury Bonds) are at a rate of approx. 2,6 – 2,8%, but they bear the totally unpredictable risk of the currency itself, the US Dollar. The same goes for all USD-based financial products.

Investing in company shares is recommended rather for the short term, as the value of company shares highly depends on the skills and luck of the management of companies, and on the sentiments of the market, of investors.

Shares, as all other financial products, do bear a counter liability, the liability of fulfilment by the issuer. Investing in financial products of any kind always also means investing in the liability of others.

More conservative people, who aim to preserve their wealth on the long term, prefer fundamental assets in their portfolio. There is almost no wealth management firm in Switzerland and no private banking department of Swiss banks that does not recommend their clients to have a hold a substantial part of their assets in physical gold.

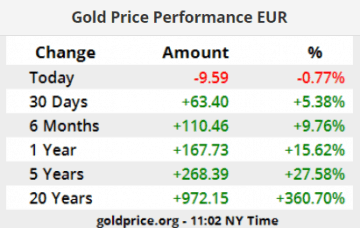

Comparing with the loss and interest figures in above paragraph headed “Cash on current account creates losses”, people who did hold physical gold in their portfolio, preferably held outside the banking system, were and are on the sunny side of life. Here is a table of physical gold yields during the last 20 years (as per 01/ß7/2019):

Many good reasons for gold:

There are many good reasons to keep wealth in form of physical gold:

- Gold is not exposed to counterpart risk. Gold has an inherent value. What one holds in his/her hand is the value itself.

- Gold cannot be debased like money, which may be subject to depreciation.

- Gold cannot be produced by governments as they print money when they need it. The scarcity of gold is protecting its value.

- Gold has no default risk.

- Gold is not exposed to banking risks if stored outside of the banking system.

- The holder of gold is the legal owner of his/her gold, if stored in the right way and with the right custody partners. In contrast, when investing in financial products, the investor is not the legal owner of anything, but the owner of promises made to him/her.

- Gold is a liquid asset, as liquid as money is.

- Gold is globally accepted, and no exchange rates apply as they apply for different currencies.

- Gold can well be used as a collateral for loans (so-called Lombard loans).

- There is no tax on gains from gold, if held for at least one year. This is the case in Cyprus, in most EU countries and in many other countries.

Should you be interested in purchasing physical gold and storing it safely outside the banking system in your own name, in sophisticated high-security storage facilities in Liechtenstein, please contact us for further information.

We do not offer investment advice:

This information is provided solely for general information and educational purposes. It is not, and should not be construed as, an offer to buy or sell, or as a solicitation of an offer to buy or sell.