Gold In The Changing International Monetary System

By Dr Tatiana Fic, Director, Central Banks and Public Policy, World Gold Council for the Eurasian Financial & Economic Herald.

The changing international monetary system

Economic power is shifting from West to East. China is now the world’s largest economy on a purchasing-power parity basis. It is the largest trading nation in the world and has the third largest sovereign debt market. Over the last decades China has become a key driver of global growth and it will continue to propel the world economy over the years to come.

The reconfiguration of the structure of the global economy and China’s rising global footprint is likely to have an impact on the international monetary system, with the greater use of the Chinese currency as one of the forces shaping the global financial system. The international monetary system is likely to move away from the unipolar, US dollar – based system towards a multipolar system, with not only the US dollar, but also the euro and potentially the renminbi playing the role of the main reserve currencies.

Since 2009 the Chinese authorities have introduced a number of measures aimed at promoting renminbi cross border settlements, including building an offshore renminbi market and facilitating access of foreign investors to the Chinese bond market. Since the inclusion of the renminbi into the SDR basket, the share of the renminbi in international reserves has surpassed those of the Australian dollar and the Canadian dollar and currently it stands at 1.95% (as of Q1 2019). The inclusion of Chinese bonds into the global bond indices earlier this year will provide a further impulse for investment into Chinese bonds and will further expose foreign investors to the Chinese sovereign bond market.

The renminbi’s use in international trade will most likely increase further once certain conditions are fulfilled, most notably those regarding the currency convertibility and the continued opening of China’s capital account. The real question is not whether this will happen, but when and what regions are likely to adopt the renminbi as one of their main reserve currencies. While it will be difficult for the renminbi to rival the US dollar as the global currency, Asia seems to be the natural habitat for the renminbi (Eichengreen, Lombardi, 2017).

As the international monetary system transitions from the unipolar, towards a multicurrency system, gold, as a safe haven asset and a hedge against financial shocks and currency crises, has remained and will continue to remain an important element of central bank portfolios.

Recent trends in central bank gold buying

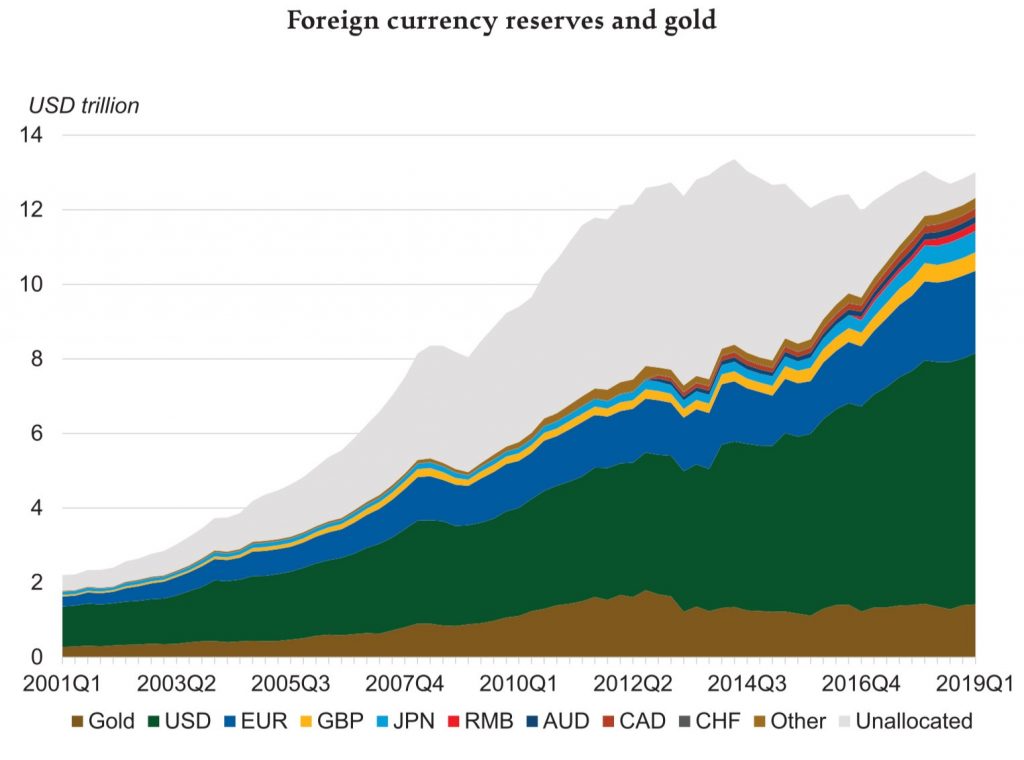

Over the past decade, central banks have purchased more than 4,300 tonnes of gold, bringing their total holdings to nearly 34,000 t. Following the USD and EUR, gold makes the third largest reserve asset in the world, constituting about 11% of world’s international reserves (chart 1).

Chart 1 | Source: IMF, World Gold Council

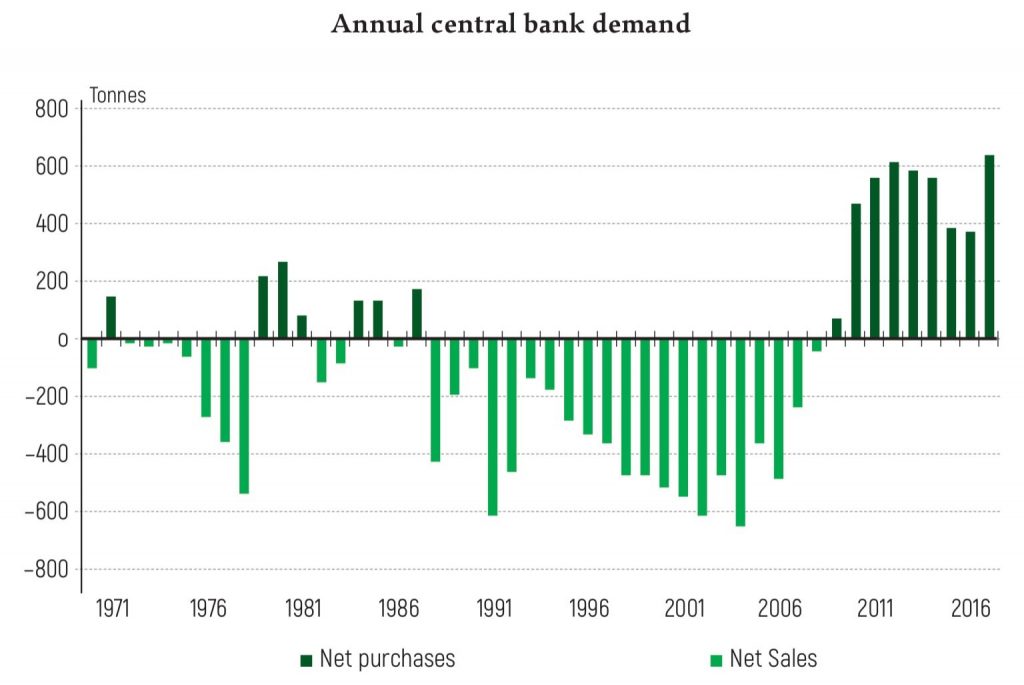

Since the global financial crisis central banks have remained firmly on the gold purchasing pedal, with central bank gold demand fluctuating at about 500-600 tonnes per year (chart 2).

Chart 2 | Source: Metals Focus, Refinitiv GFMS, World Gold Council

Last year central bank purchases of gold totalled 651 tonnes – more than at any time since the end of Bretton Woods and the suspension of US dollar convertibility into gold nearly 50 years ago.

The vast majority of buying has come from developing country central banks. Russia, China, Turkey and Kazakhstan have been the largest purchasers. The share of gold in developing country central banks remains relatively low. The overall allocation is 5% as compared to 16% for advanced economies which may suggest there is scope for further growth. At the same time, over the past decade the advanced economy central banks stopped selling gold under central bank gold agreements. Earlier this year, they decided not to renew the agreement upon its expiry in September 2019. In the press release issued by the ECB in July, 22 signatory central banks confirmed that none of them currently has any plans to sell gold. The signatories stated that gold remains an important element of global monetary reserves.

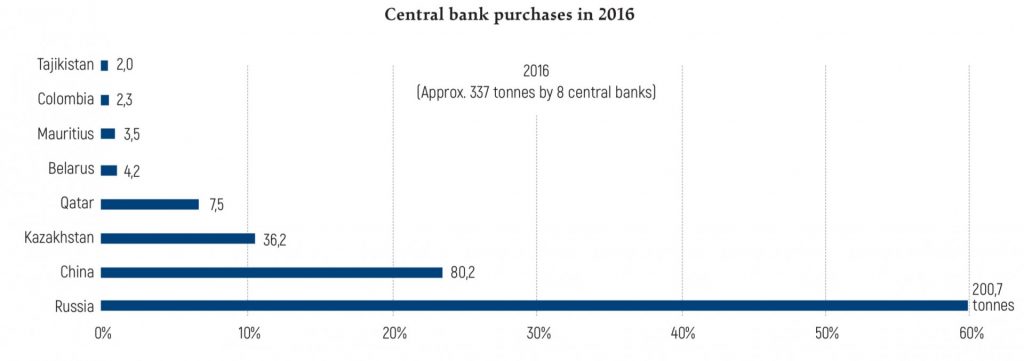

While the developing country central banks have been active purchasers, the pattern of demand has changed in recent years. In 2016, demand was highly concentrated in Russia, China and Kazakhstan (chart 3a).

Chart 3a

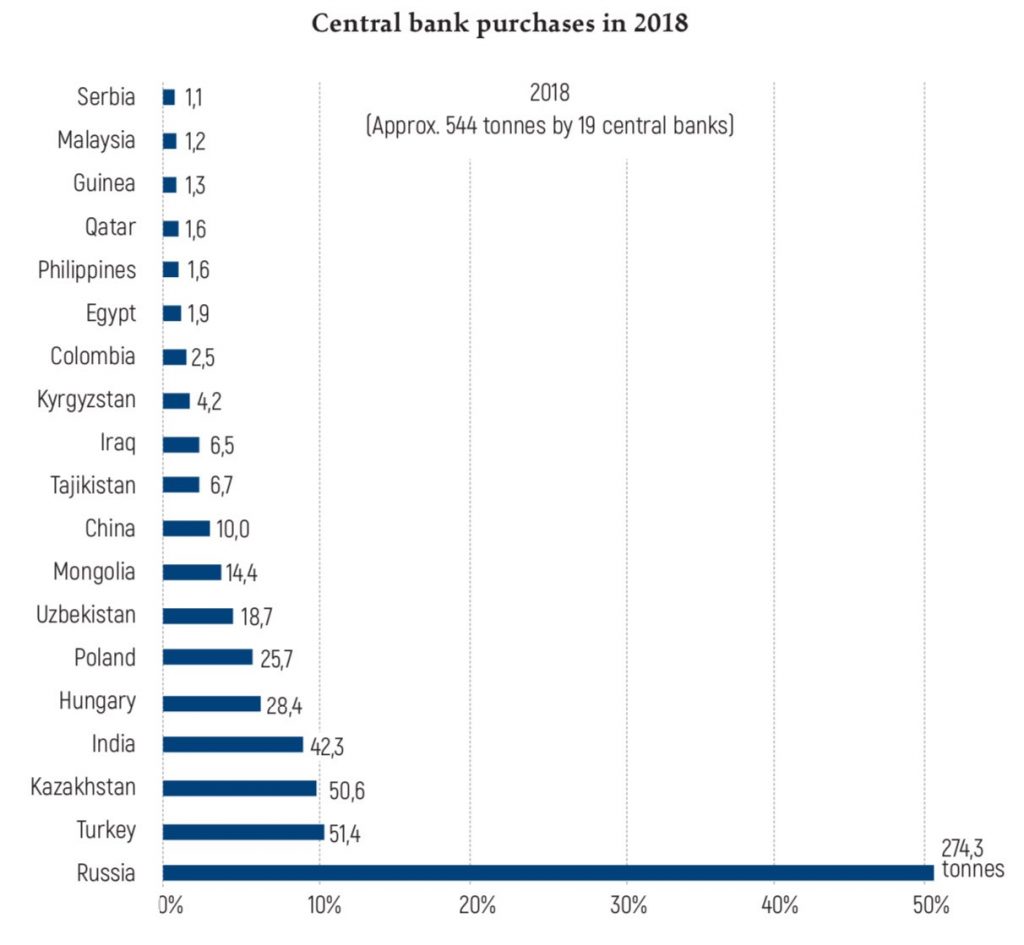

By 2018, the demand had become far more diverse, with nineteen individual central banks buying over one tonne of gold last year, according to IMF data. Countries that had been absent from the gold market for many years became notable buyers of gold. The European Union re-emerged as a net buyer, after substantial purchases from Poland and Hungary (Chart 3b).

Chart 3b | Source: IMF, World Gold Council

Factors driving central bank gold demand

Central banks hold gold for various reasons – as a strategic asset, to satisfy their objectives of ensuring international reserves liquidity and security, and to diversify their reserve portfolios. Gold is especially well suited to central bank reserve portfolios whose principal function is to protect the country against external shocks. The negative correlation of gold with other assets allows central banks to maximise the return on their portfolios, at the same time minimising the risks.

The recent increase in central bank gold demand has been driven by a combination of macroeconomic and geopolitical factors, as well as structural changes in the global economy.

Macroeconomic uncertainty resulting from deteriorating budget positions, and rising debt of some of the reserve currency countries, an increased threat of currency wars, and protectionist policies have prompted central banks to diversify their portfolios.

Some of the central banks buy gold at the same time reducing their US Treasury holdings. The dedollarisation of reserves is a response to sanctions and increased political tensions.

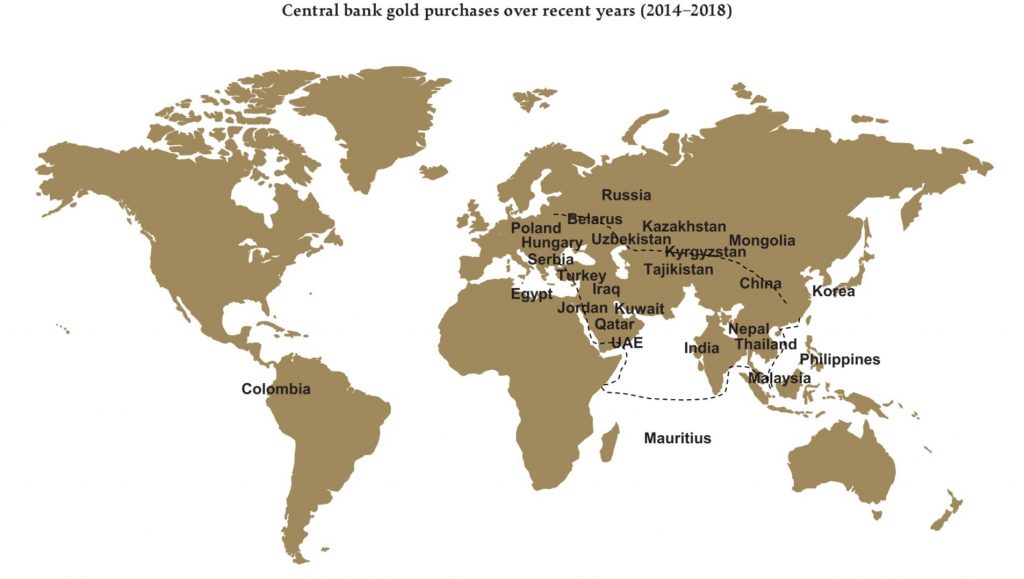

Some central bank purchases reflect a desire to hedge against future changes in the international monetary system. It is noteworthy that most of the recent gold purchases have been coming from countries with strong trade and investment links with China in Southeast and Central Asia (chart 4).

Chart 4 | Source: Metals Focus, World Gold Council

The rising exposure of the Belt and Road countries to China will likely result in higher holdings of the Chinese currency in their central bank reserves in the future. As the process of full regionalisation of the renminbi will take time, these countries have been purchasing gold instead. As the shift to a new international monetary system could be both destabilising, due to hot money flows and changing expectations, and possibly weigh on the US dollar, gold can serve as a hedge against both.

GOLDHUB

Enhancing trust in gold through data

“Credible data is critical to the informed investor, so we take pride in seeking to source the highest standards in the data we provide. Building on our existing data series, using data from public and commercial third parties, we have created a comprehensive information resource for gold as an asset class.

Alongside data, our new website brings together our expert research and interactive tools in one accessible and easy-to-use location. The Goldhub research library gives you access to a wealth of material on the role, drivers and performance of gold as an asset class from industry experts. Whether looking for data analysis and context, the latest updates or a deeper understanding of the gold market, Goldhub is a rich resource to support strategic asset management. Visual analytics and data downloads also allow you to engage with gold market data, helping you to verify and develop your own insights.

Usability, breadth of data and depth of knowledge make Goldhub equally relevant to asset owners with existing positions in gold and those who are new to the asset class. For the former, relevant data is readily available; for the latter, Goldhub provides information and guidance on gold’s value as a strategic asset.

As the site develops, more data and insight will be added to provide even greater levels of transparency and understanding around the value of gold as an asset class. In March, we launched the Goldhub blog, which features market insights from our teams across the world, as well as external commentators who provide a unique perspective on aspects of the market.”

This article is republished on our website with the kind permission of the World Gold Council. Details about the author of this article:

Dr Tatiana Fic, PhD

Director, Central Banks and Public Policy,

World Gold Council

Tatiana was formerly a Research Fellow at the UK National Institute of Economic and Social Research, working on projects related to the work of the United Nations and the European Commission. Prior to that, she held various positions at the National Bank of Poland, including as Head of the Macroeconomic Projections Division. Tatiana holds an MSc in Quantitative Methods and Information Systems, an MSc in Finance and Banking, and a PhD in Economics from the Warsaw School of Economics.

View the September issue of the Eurasian Financial & Economic Herald here.

___

LIEMETA ME Ltd

LIEMETA ME Ltd, Nicosia, Cyprus, provides physical storage of precious metals at its prime location in Liechtenstein as well as trade services of precious metals, mainly gold, silver, platinum and palladium.

Your precious metals are safely and securely stored “segregated and allocated” and we are one of the few physical storage houses for precious metals that provide full-cover insurance, including embezzlement.

Stored assets are fully legally owned by the client, client assets are of course not on our companies’ balance sheets.

LIEMETA is a privately owned, independent and non-bank company, meaning that its services do not fall within the scope of CRS or AEOI.

LIEMETA provides 100% discretion, 24/7 access to clients’ stored assets at its sophisticated unit and high-security building.

LIEMETA is proud to be chosen by high net-worth individuals as their trustworthy custodian, in Liechtenstein.

You are welcome to contact us through the below contact form.

We do not offer investment advice:

This information is provided solely for general information and educational purposes. It is not, and should not be construed as, an offer to buy or sell, or as a solicitation of an offer to buy or sell.T