Gold market analysis on November 2021

Based on the LBMA reference price, gold increased 2% in November, gaining early in the month before giving up most of its gains in the following weeks. Gold’s performance was influenced by weaker equities and commodities, lower rates, and the strength of the US dollar.

Several important moves highlighted the trend of the gold price in November:

Gold rose from an intra-month low of US$1,763/oz on November 3 after the US Federal Reserve revealed its intention to taper its bond-buying program while delaying rate rises. The surge in gold was accelerated when the BoE surprised markets by keeping interest rates unchanged.

A few days later, the October US CPI reading of 6.2% y-o-y — the highest level since 1990 – fuelled fears that inflation might be more persistent than initially expected. This increased the gold price by $30/oz, bringing it close to $1,860/oz.

Gold’s escape from a 15-month downtrend proved short-lived, as positive US retail sales prompted the US dollar to gain more, generating headwinds for gold. This was compounded by rising yields in the aftermath of Fed Chair Powell’s re-election.

Gold found support at its 50- and 200-day moving averages near the end of the month at $1,780/oz. In the closing days of November, fears over the new Omicron COVID variant provided some further safe-haven support for gold, but it wasn’t enough to drive gold beyond US$1,800/oz.

Price performance was mirrored by changes in net long positioning on the COMEX. Net long positions increased to 882t (US$52bn) in the first half of the month, the biggest tonnage level since early August 2020 – around the time the US$ gold price touched a new high of US$2,067/oz. Managed Money traders, on the other hand, reacted to Powell’s re-nomination by reducing their positions to 731 t (US$42 bn) at the end of the month, in line with the price fall.

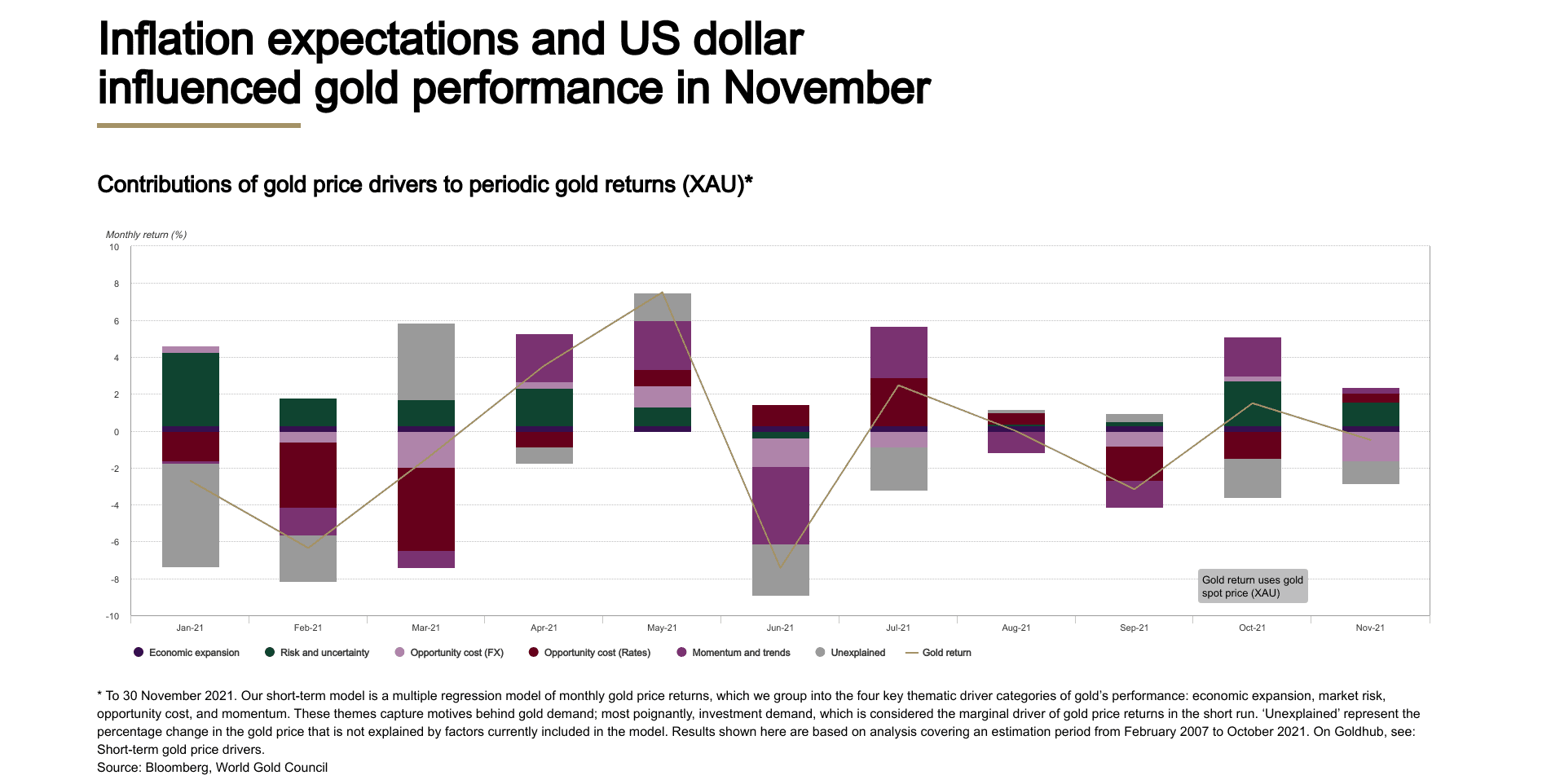

The return attribution model shows that the rising US 10-year breakeven inflation rate was the dominant positive factor for gold, pushing real yields lower for much of the month, which is consistent with qualitative evidence. Intra-month, breakeven inflation climbed to 2.7%, its highest level since 2005, before falling back to 2.5%. Investors’ persistent concern on the course of inflation (in the US, but also globally) and the Fed’s and other central banks’ potential responses continues to impact gold prices. Dollar strength, on the other hand, was a headwind in November, dragging gold’s performance down, but not enough to outweigh inflation concerns.

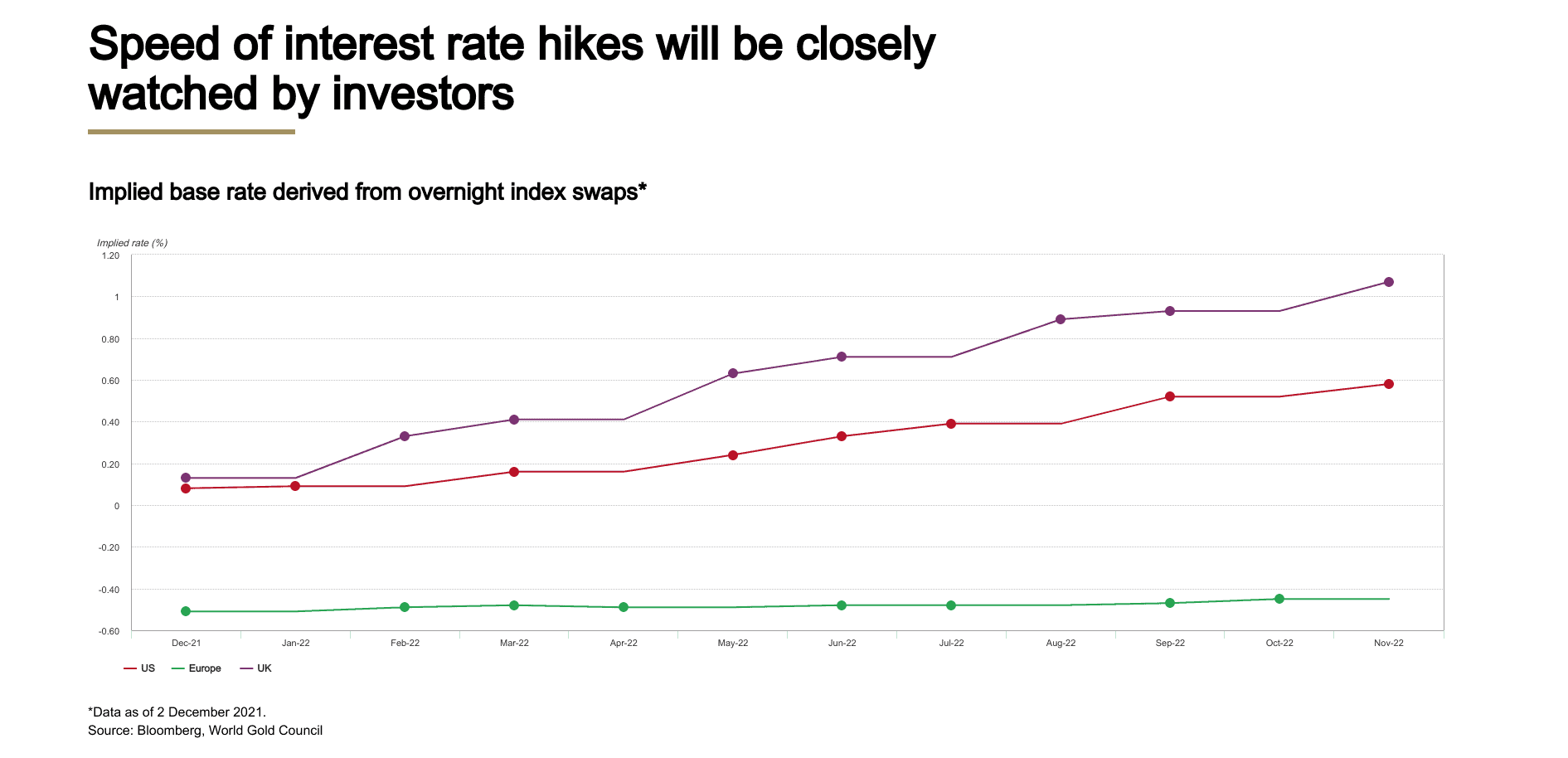

For the rest of the year, investors are likely to be obsessed with inflation and the probable monetary policy reaction. Chairman Powell has remarked that the term “transitory” should no longer be utilized and hinted that the Fed may begin tapering sooner than previously thought. As new economic statistics are presented, market participants will likely continue to try to predict the Fed’s intentions. Both the ECB and the BoE have policy meetings in December, but market expectations differ: the ECB appears committed to its accommodative position, whereas the latter may tighten sooner. These decisions will almost certainly continue to drive gold prices.

COVID is also a constant source of ambiguity. Increased cases have led to the reimposing of restrictions in many regions of Europe. And the new Omicron variant adds to the strain. While there are more concerns than answers, it’s worth noting that many of the recent 2022 prognosis studies haven’t identified new COVID-19 variants as a threat in the coming year. Omicron also emphasizes that the pandemic’s risks have not yet disappeared. And it may cause institutional investors to think again about their downside protection.

Many of the factors that have drove gold this year, including as the pace and direction of inflation and rates, COVID, and the resilience of global economic growth, we believe will continue to be relevant in 2022. Uncertainty will almost certainly continue to encourage gold investing as a hedge. Likewise, the strength of consumer demand recovery will be determined by the strength of economic recovery in key markets, as well as the direction and volatility of the gold price. Finally, because gold is a crucial component of central bank reserves, we predict continuing support from central banks.