Gold Market outlook 2022

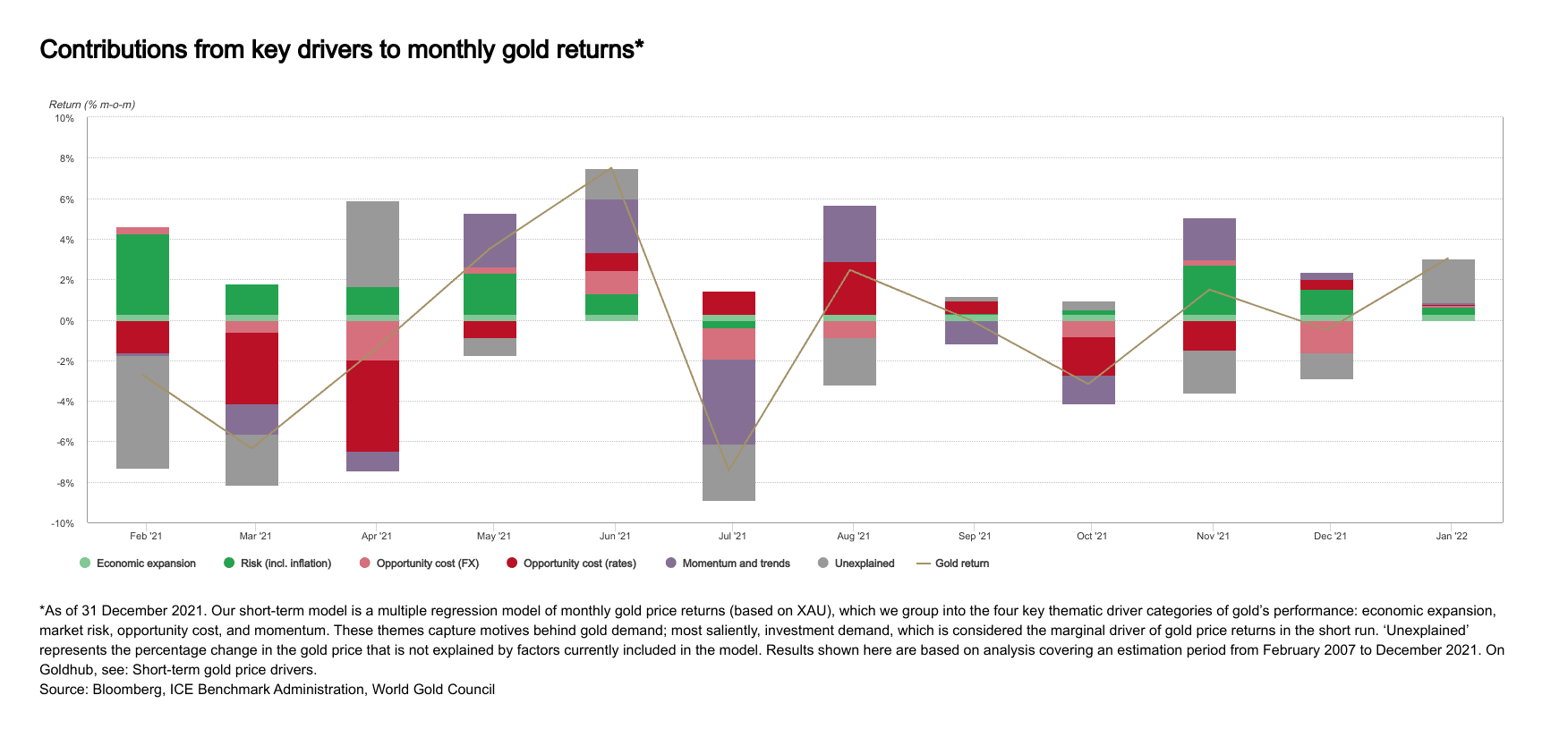

Gold completed the year at US$1,806/oz, down around 4% from the previous year’s close. On the heels of the fast-spreading Omicron variant, the gold price rebounded through the end of the year, possibly prompting flight-to-quality flows, but it was not enough to balance H1 weakness.

Investor optimism likely fuelled a drop in portfolio hedges in early 2021, as newly developed vaccines were rolled out. This had a negative influence on gold’s performance and resulted in withdrawals from gold ETFs. The remainder of the year was spent in a tug-of-war between opposing factions. Uncertainty about new variants, combined with rising fears of high inflation and a rebound in gold consumer demand, pushed gold forward. Rising interest rates and a stronger US dollar, on the other hand, continued to be headwinds. In other local currency terms, such as the euro and the yen, however, dollar strength resulted in positive gold returns.

Rising opportunity costs were a major factor in gold’s negative performance in Q1 and occasionally in H2, but rising risks – particularly those associated with rising inflation – pushed gold higher toward the end of the year.

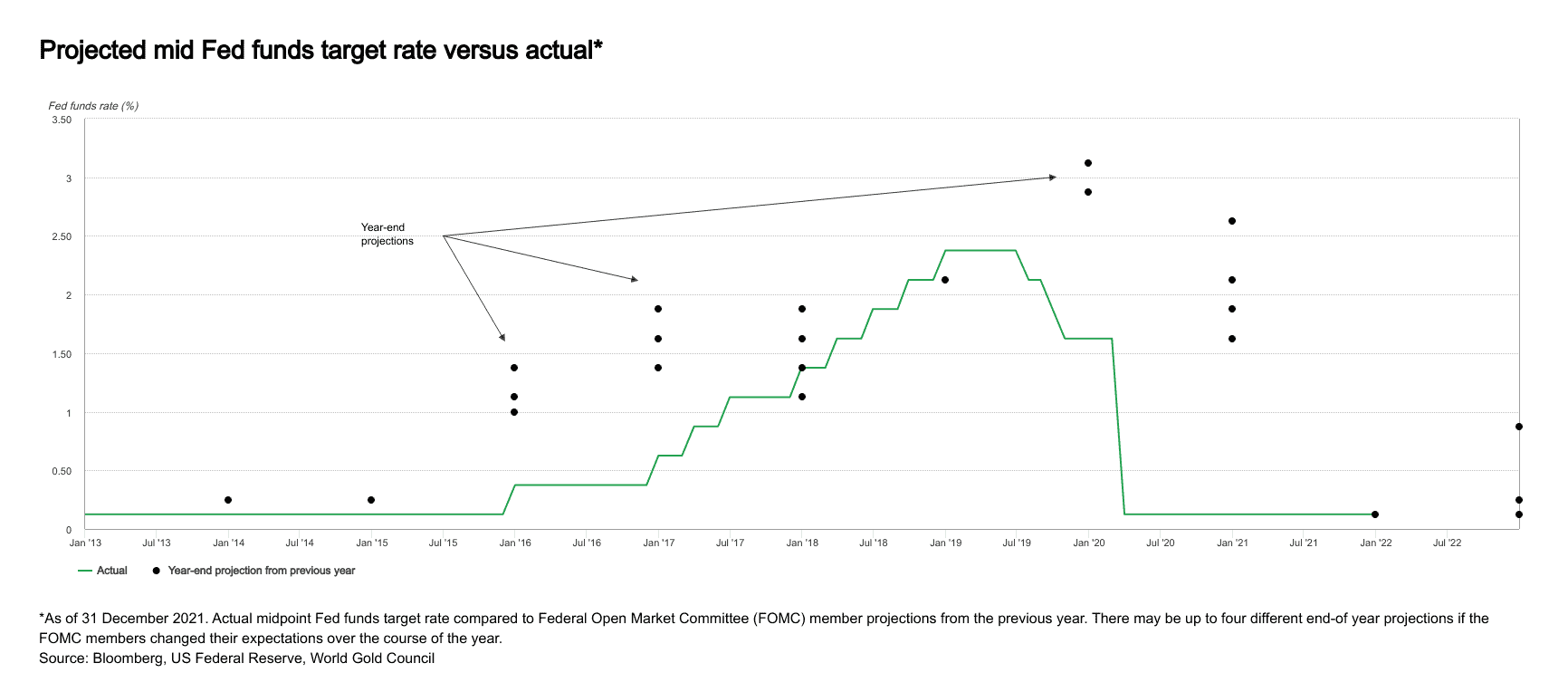

The US Federal Reserve is signalling a more hawkish stance as we enter 2022. According to its predictions, the Fed will hike three times this year, faster than previously projected, while aiming to shrink the size of its balance sheet. However, a study of previous tightening cycles reveals that the Fed is tended not to tighten monetary policy as aggressively as members of the committee had anticipated.

Dot-plot forecasts show that Fed expectations for the 2022 have notably outperformed actual target rates. However, financial market expectations of future monetary policy measures – as indicated in bond yields – have traditionally had a significant impact on gold price performance. As a result, gold has historically underperformed in the months leading up to a Fed rate hike, only to gain strongly in the months following the first-rate hike.

The US dollar, which displayed the opposite pattern, may have supported gold to some extent. Finally, ahead of a tightening cycle, US equities had their best performance, but subsequent returns were lower.

Finally, while the relationship with US interest rates receives a lot of attention, gold is a global market. And not all central banks are as swift as the Federal Reserve.

For example, despite recent record inflation figures, the European Central Bank has warned that raising interest rates in 2022 is “very unlikely”. While the Bank of England raised interest rates in December, the Policy Committee appeared to indicate only modest future rises.

The Reserve Bank of India has also indicated that it will retain its supportive monetary policy stance in order to boost and sustain economic recovery and limit COVID’s impact. In December, the People’s Bank of China cut one of its policy rates by 5 basis points, just a few months after decreasing the required commercial banks reserve ratio to cushion the country’s economic decline.

While diverging monetary policies may result in a stronger dollar, regional gold investment demand should be supported by steady or lowering rates.

Gold and Inflation Rate

When inflation is high, gold has historically performed well. Gold’s price increased 14% on average in years when inflation was higher than 3%. Furthermore, throughout time, gold has outpaced US inflation and has moved closer to the money supply, which has expanded dramatically in recent years.

There are several reasons that cause inflation to remain high, for instance:

- Supply-chain disruptions from the initial COVID wave, as well as subsequent dislocations as new variants arise;

- Tight labour markets, which, in combination with COVID fatigue, have boosted the number of workers looking for new, better-paying jobs;

- Higher average savings starting in 2020, which has contributed to soaring financial market valuations;

- Soaring commodity prices.

Despite the possibility of rate hikes by some central banks, nominal rates will remain historically low. Even more so, rising inflation is likely to keep real rates low. This is significant for gold because real rates, which combine two fundamental determinants of gold performance: “opportunity cost” and “risk and uncertainty,” frequently respond to gold’s short- and medium-term performance.

Low interest rates, both nominal and real, are also pushing investment portfolios toward riskier assets. As per one of the recent studies, this, in turn, increases the demand for a high-quality liquid asset like gold.

Factors Linked to Gold’s Price Behaviour

Gold’s price behaviour is frequently considered to be linked to investment demand, particularly from financial instruments like gold ETFs, over-the-counter contracts, and exchange-traded derivatives. That, is just partially correct. Variables connected with these forms of gold investments, such as interest rates, inflation, currency rates, and, more broadly, flight-to-quality flows, tend to respond to shorter-term and more significant price swings.

However, analysis shows that gold’s performance is also influenced by other factors such as jewellery, technology, and central banks. While these do not usually result in the big price swings associated with investment, they do contribute to support or create headwinds for gold price performance.

During 2022, gold is expected to confront two major headwinds:

- Higher nominal interest rates;

- Possible strengthening of the dollar

However, other supporting variables may offset the negative impact of these two drives, such as:

- High, persistent inflation;

- Market instability caused by COVID, geopolitics, etc;

- Strong demand from other sectors such as central banks and jewellery.

In light of this, gold’s performance in 2022 will be determined by the factors that tip the scale. Gold’s value as a risk hedge, on the other hand, will be particularly relevant for investors this year.