Gold: Outlook 2020 and the Impact of Reserves

Gold has been on an upswing in recent months, and it looks like 2020 could be a positive year for the price action of the yellow metal. The conflict between the US and Iran has been cited as an important driver for gold prices, as the metal acts as a hedge against geopolitical risk. While this is no doubt supportive of gold prices, there is another factor that could be much more important to gold’s price in the medium and longer term.

Negative interest rates are becoming more common, and depending on how it is measured, as much as 90% of the developed world’s government bonds are trading with negative real interest rates. The simple fact is that fiat currency no longer offers much in the way of a return for those holding it, especially for institutions that have to consider counterparty risk when buying assets.

Global central banks have been major buyers of gold over the last 18 months and have bought more gold than in any period since the ‘Brown Bottom’ that occurred around the year 2000. In addition to the low-to-negative interest rate environment, China’s expansion into Eurasia seems to be pushing gold back into the position of a monetary reserve asset.

The US dollar is still widely used as a reserve asset by central banks, which may be one of the factors that puts a floor under the gold price in this decade. Many nations are moving away from their economic reliance on the West and opening their economies up to Chinese investment. Gold has a heritage in China that goes back millennia, and it appears that China would rather see gold take the place of the Yuan/Renminbi (RMB) as a reserve and settlement asset.

The US Dollar’s Continued Popularity is Curious

It might seem strange that the US dollar is still used as the primary reserve asset by central banks globally. The US dollar still accounts for more than 60% of global reserve assets, even though the USA has been at the centre of a trade war that threatens to sink the world into a recession.

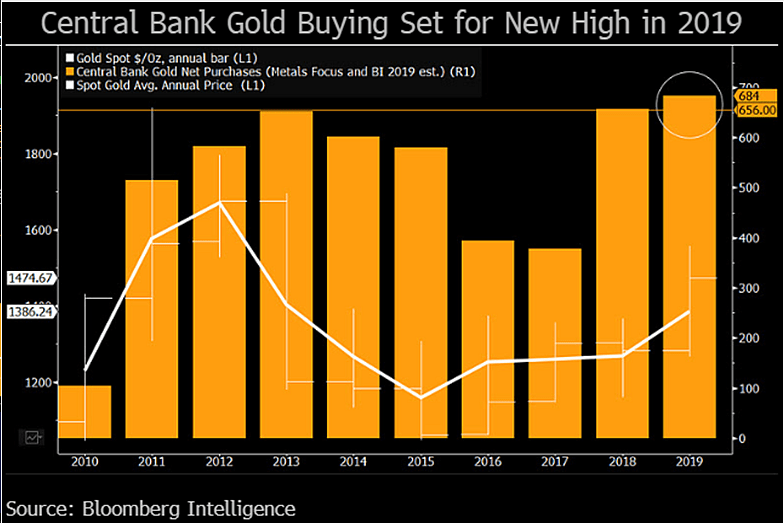

It should come as no surprise that central banks are shifting their currency reserves, US dollars included, into gold. In the first half of 2019 global monetary authorities bought more than 374 tonnes of gold. During the rest of 2019, central banks continued buying gold, and the yearly total purchases of gold by central banks totalled 684 tonnes, surpassing record gold purchase in 2019, which were 651 tonnes. Central Banks’ gold purchases 2019 were the highest since 1971.

Hungary’s purchases of gold in 2019 were the highest in 30 years, while the Reserve Bank of India (RBI) added to the amount of gold that it buys on the open market for the first time in a decade. The gross amount of gold purchased by central banks and monetary in authorities in 2019 rose by 17 tonnes over the previous year, which had been a 50-year record high.

The current popularity of the US dollar as a reserve asset is likely to support gold in US dollar terms going forward. Central bank gold buying is likely a way to divest US dollar reserves, as the global reserve asset has low-to-no yield in real terms, and rising political risks attached to it.

The gold buying that occurred in the first half of 2019 represented a year-on-year rise of 57%. To be sure, the decline of US popularity in the geopolitical arena isn’t the only reason why gold buying by central banks and other monetary authorities is rising. China appears to be promoting the use of gold as a reserve asset, and not pushing to internationalize its currency as a means of settlement.

China’s Eurasian Push Looks Positive for Gold Prices

China is in the middle of the biggest international infrastructure program in history. The Belt and Road Initiative (BRI) is a Chinese state-sponsored program that seeks to connect China to Eurasian markets, and global natural resources with China. The BRI is being funded by Chinese entities both public and private, with billions of RMB flowing into nations across planet.

It would be natural to assume that with the advent of BRI funds flowing offshore, the RMB would become a more widely used reserve asset, and also a means of international payment. This is not the case, as most BRI funds are ‘sent’ in the form of RMB loans, which are then spent directly back into the Chinese economy.

There is no way to know if China is intentionally supporting the role of gold in the Eurasian financial market, but the net effect of China’s resistance to push RMB usage outside of bilateral deals leaves numerous central banks with a dilemma: continue to hold USD and EUR, or shift reserve assets to gold?

On the central bank gold buying side, we see that numerous BRI-linked countries are buying gold. Over the last five years Kazakhstan, Uzbekistan, and Turkey have been among the top 10 largest buyers of gold for central bank reserves, with Russia and China holding the top two positions for both the last five and ten years.

It isn’t difficult to see that gold is taking on a larger role in the Eurasian financial system and that this trend is likely to support gold prices in US dollar terms. China no longer has the desire to accumulate US debt in the way it did over the last few decades. In fact, Japan overtook China as the largest holder of US sovereign debt in 2019, though both nations are shedding US government debt on a gross basis.

Geopolitical Risks Support Safe Haven Assets

There are numerous risks to geopolitical stability, all of which support gold prices. The recent assassination of Iranian General Qasem Soleimani demonstrates how a seemingly benign geopolitical threat can quickly metastasize into a regional conflict. For the moment the worst has been averted, but no major change of direction of the conflict has been achieved.

US President Trump has added sanctions to another Iranian General, who is being accused of killing Iranian protesters. Iran has removed any limits to its uranium enrichment program, which isn’t going to create a positive environment for negotiations or de-escalation. Iran isn’t the only hotspot on the globe, and any number of events could upset the fragile geopolitical balance.

In this environment of rising risks, central banks, investment professionals and traders face a new challenge. One of the traditional safe-haven assets, government bonds, may not be safe anymore.

Global conflict has been bullish for government bonds in the past, but today, the US is at the centre of a conflict that could easily shatter the value of the US dollar. Any issues with the US dollar’s value would eliminate the role of US debt as a low risk asset and plunge the global financial markets into chaos. There is no way to assign a probability to these sorts of events, but the conditions for a major FOREX dislocation are in place.

New Reserve Assets are Emerging

The role of gold as a reserve asset in the West is limited, but many other regions are quickly adding gold to central bank or other official state reserve assets. Even in the absence of further geopolitical risks, central banks across Eurasia are likely to continue to add gold to their official reserves. China’s rise to economic power has not seen the RMB challenge the USD, which leaves many nations with difficult choices.

For the moment, it appears that many central banks are opting to slowly turn their USD reserves into gold. Whether or not gold will regain the role that it had in the global monetary system is unknowable. The yellow metal may be a ‘golden bridge’ to a multipolar financial system with a range of reserve currencies, or it may once again be the material that underpins social faith in the money supply.

The next few decades will answer these vitally important questions, for 2020, it would appear that gold is in a good position to maintain its present value due to central banks diversifying away from the USD. Gold may rise substantially from current levels if there is a geopolitical crisis or FOREX dislocation that involves the USD.

We do not offer investment advice:

This information is provided solely for general information and educational purposes. It is not, and should not be construed as, an offer to buy or sell, or as a solicitation of an offer to buy or sell, or as investment advice in general.

Interested in buying and storing gold?

Please contact us through the form below and we will be happy to revert to you.