Gold supply chain flexibility amongst interruption

The gold supply chain precised into bars and coins in various countries is distributed worldwide. This geographical dissemination leads to stability and demand satisfaction. However, COVID-19 pandemic has caused remarkable interruption to various parts of the gold supply chain which we will analyse on how different components across the supply chain have been affected, on the impact on the gold flow through the supply chain and on the effect on the investment demand.

Nevertheless, despite the fact that the gold supply chain was harmed by the pandemic, it still has shown resilience in the face of these challenges and highlighted a key strength of the market and stability.

The gold supply chain with its components enables the smooth functioning of the gold market with allowing the gold to flow where needed and in the desired form.

Strained supply sources

Gold mining is geographically distinct and was indeed affected by the pandemic but this dispersion has helped to safeguard the primary gold supply from more severe outcomes.

Main mining nations like China for example, saw mining activities decreased but these production declines were balanced by more consistent production levels in other major mining regions that had less operation disruptions.

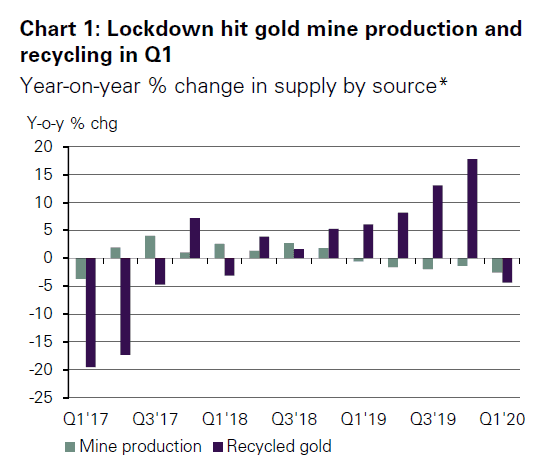

Total gold production fell 3% y-o-y in Q1 which was a relatively moderate decline given the scale of the pandemic. Some mining countries had to extend into Q2 but they are all gradually easing with slowly boosting up the production.

Recycling activity was also affected in Q1, falling 4% y-o-y which was the lowest level in 2 years. (Chart 1)

The 6% rise in the US Dollar gold price during Q1 would normally have drawn out near market supply but this was weakened by the lockdown measures worldwide. The physical exchange of gold for cash was waved and consumers were instructed to take security in their homes and jewellery retailers were closed down temporarily which reduced the amount of gold onto the market.

Downstream capacity was reduced

Refinery operations were halted and the consequent reduction in global refining capacity meant that bars and coins couldn’t be produced as needed. However, in contrast to the supply chain squeeze, unaffected refineries increased production capacity in that time to meet some of the excess demand.

Logistical nightmares

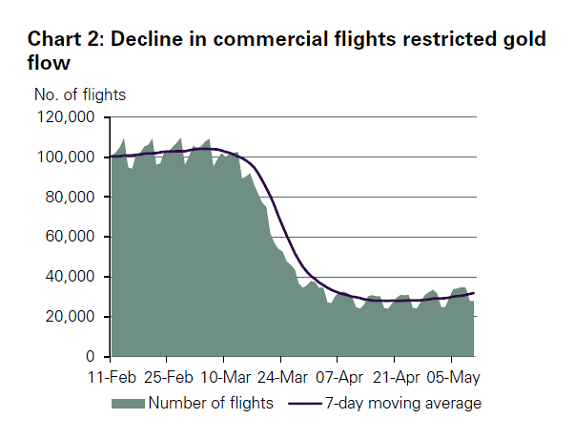

Supply chain disruption has not been focused only on sourcing and refining of gold but travel restrictions worldwide also delayed the gold flow along the chain. Gold transportation was of course negatively affected due to no transportation network, border closures, flight restrictions and in general travel restrictions leaving the supply chain looking for alternative means of transportation like chartering cargo-only aircraft.

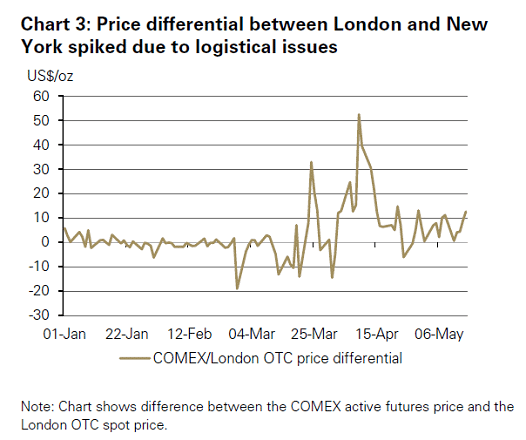

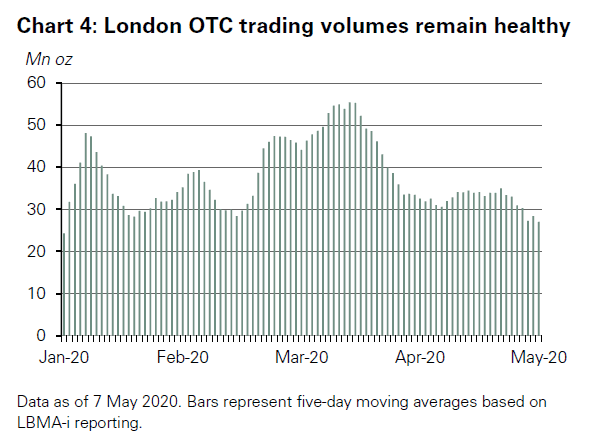

While the logistical issues have caused disruption to the free movement of gold which resulted in localised liquidity issues, overall liquidity in the gold market remained and remains booming.

Disparity in bars and coins supply

The Covid-19 outbreak took investors uncertainty to new highs against the existing global backdrop of low and negative interest rates and an anaemic growth outlook which fuelled in gold investment demand in Q1 as investors needed safe-haven assets particularly in US and Europe. Usually this demand could be met through various sources but in the current environment a disparity in the supply of LGD and retail bars and coins emerged.

Stock of LGD bars countered supply issues

In the wholesale market the availability and liquidity of LGD bars was relatively unaffected by the supply chain issues.

In contrast to gold futures on COMEX, which are linked to 1kg bars, most gold-backed ETFs (gold ETFs) are linked to LGD gold bars and these have benefited from the ample supply. In Q1, inflows into gold ETFs added up to 298t, the highest level of quarterly inflows for four years and the strong flows have continued through April and May.

This was supported by the large stock of LGD bars: at the end of January a record 8,263t of gold was held in London, valued at a record US$426bn. The stock of LGD bars enabled gold ETFs to source the gold required to back the large volume of newly created shares.

As gold volatility increased in Q1 the standardisation and deep stock of LGD bars helped maintain liquidity in the wholesale gold market, benefiting individual and institutional investors alike.

Higher premiums due to less small bars and coins

At the retail level, having market fragmentation, the story was notably different. Significant stocks of small bars (1kg or less) and coins were stranded in Eastern markets where demand was restrained throughout the quarter due to COVID-19. There were supply issues due to difficulties in transporting this gold easily and quickly to meet heightened demand in western markets.

Additionally, the availability of small gold bars and coins was further stretched due to their more complex supply chain. Small bars and coins need to be distributed throughout the globe to retailers and consumers.

Coin demand, in particular, jumped 36% y-o-y, with several mints reporting robust sales. Some dealer inventories had deficiency due to supply and logistical issues and many investors had long waiting times and high premiums. Premiums for American Eagle 1oz gold coins jumped to over US$130/oz (8% above spot), the highest level for six years, compared to an average of US$25/oz (2% above spot) over the first two and a half months of 2020. Such elevated premiums should narrow considerably since the gold supply chain matters begin to ease and anecdotal evidence seems to confirm this.

Result

Covid-19 pandemic has caused significant supply-chain disruption but temporary suspension of some mining and refining activities and strict travel restrictions created remarkable challenges to the movement of gold within the market. Nevertheless, amongst these challenges the resilience of gold supply chain has shone through. Mine production and gold recycling have declined only modestly and the depth of stock of LGD bars as well as the adaptability of market participants has supported high gold investment demand.

In recent weeks the easing of certain COVID-19 restrictions has alleviated some pressure on the supply of gold. While the dislocation between the London OTC market and COMEX remains elevated, we expect that some of the dislocations that have arisen due to supply chain matters should be reduced or even eliminated, ensuring the continued smooth and efficient functioning of the entire gold market.

This article is based on information provided by the World Gold Council.

We do not offer investment advice:

This information is provided solely for general information and educational purposes. It is not, and should not be construed as, an offer to buy or sell, or as a solicitation of an offer to buy or sell, or as investment advice in general.

Interested in buying and storing gold?

Please contact us through the form below and we will be happy to revert to you.