Gold’s performance amid current global economic environment

Earlier this month, gold surpassed US$2,000 per ounce, nearly to reach the previous high record in 2020. This time, though, it was driven by continued concerns about the war in Ukraine, rising commodity prices, and, more broadly, possible consequences for the global economy. While gold price has fallen from the highs of the first days of the month, it is still about 4% higher month-to-date.

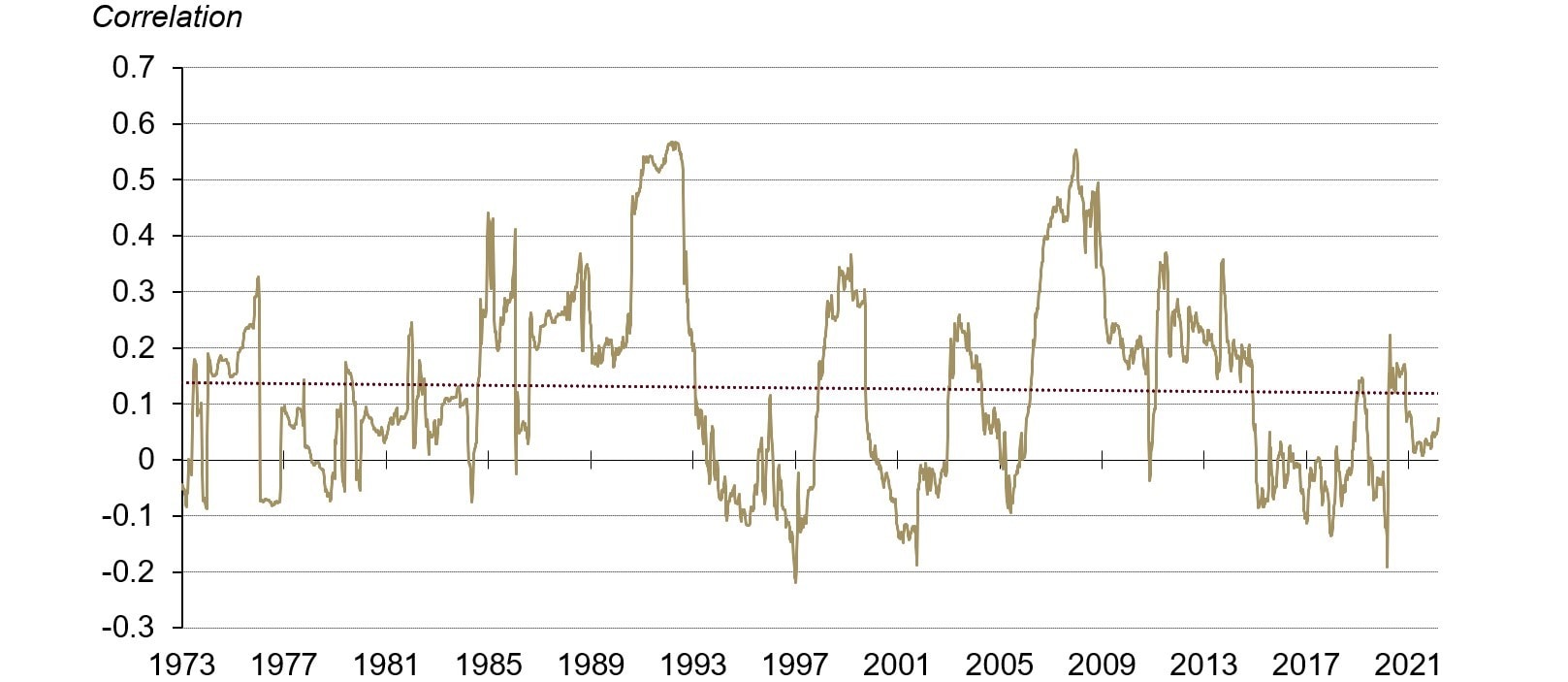

Relation between the price of oil and the price of gold

There is no consistent association between gold and oil, in general. The long-term correlation between the two assets is near to zero at any given time, ranging from -0.2 to +0.5.

However, during periods of high inflation, both gold and oil tend to perform well, even though for different reasons. High oil prices can drive up consumer price baskets, resulting in high inflation. When high inflation persists, investors seek hedges, whether it’s due to commodities or other factors, and, gold investment demand as well as gold price rises, consequently. The price of gold tends to lag the price of commodities in this case. However, gold has outperformed in the long run, historically.

Therefore, while oil price does not “cause” the price of gold to rise or fall, the economic environment that leads to an increase in oil price can also lead to higher gold price.

The war in Ukraine is an example of such an environment, as it is the result of a geopolitical event that is likely to have large economic consequences, as well as an impact on energy prices, other commodities, and supply-chain disruptions in general.

In recent weeks, commodities prices have climbed at an exponential rate. While this could continue if the war continues, any possible resolution could cause crashing down the prices. Even if gold experiences a price correction, it wouldn’t see the same level of volatility. Gold supply has not been disrupted to the same extent as other commodities, and in any case, huge above-ground stocks and much higher physical gold trade volumes, reduce the impact of newly mined supplies.

Source: Bloomberg, ICE Benchmark Administration, World Gold Council

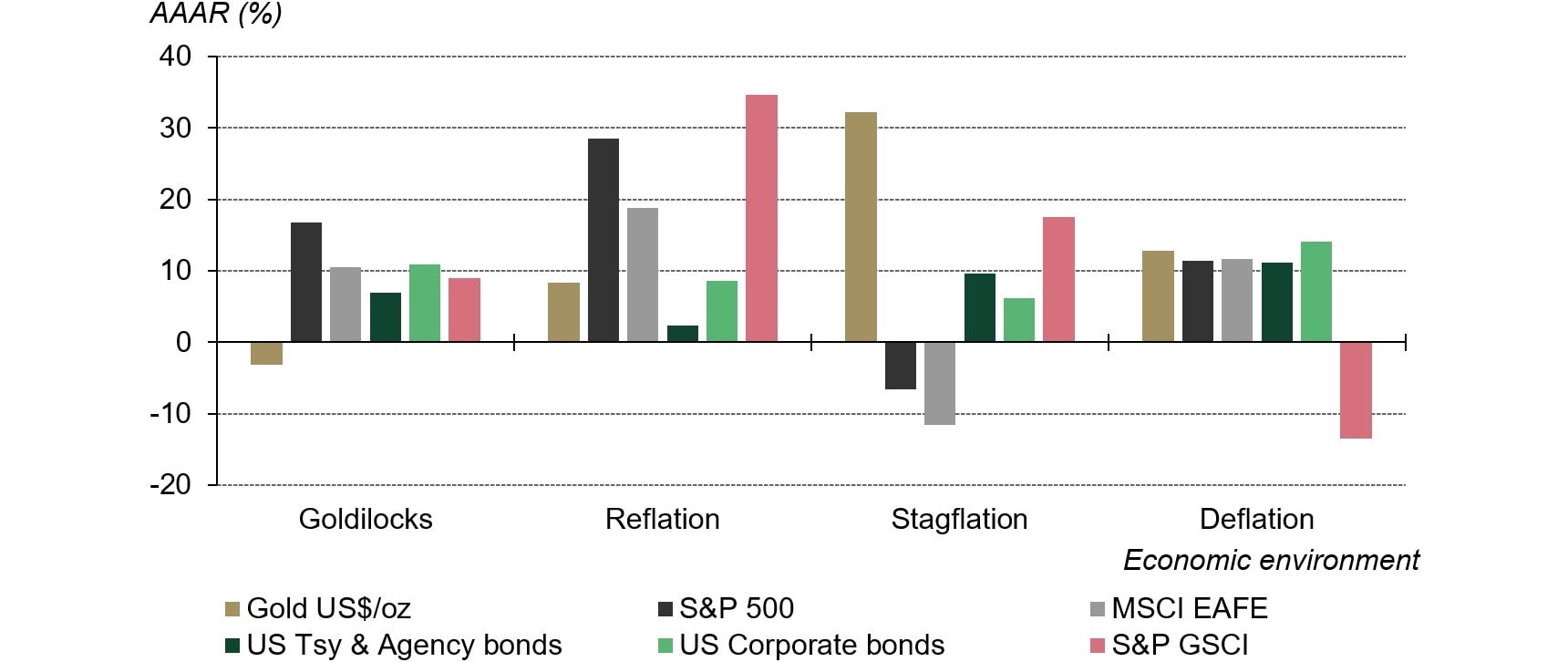

Gold performance in case of stagflation of the global economy

The possibility of stagflation is increasing all throughout the world. Europe may be the most affected, as a result of skyrocketing commodity prices, energy dependency, and a weaker economic and financial environment, all of which has been intensified by the war in Ukraine.

While stagflation is also a risk in the United States, it may not be as severe as in Europe. The US economy is resilient, according to economic data. On the other hand, if the spread between long and short maturity US Treasury bonds, as a historically reliable economic indication, continues to flatten or reverses, market investors may be anticipating a recession down the line. Stagflation risks may be realized if energy and food prices remain high.

Stagflationary circumstances, of course, are not good for financial markets or the economy. Slowing incomes and rising prices are, to say the least, an unpleasant combination. Historically, stocks are hit hardest, while commodities and gold have done well. In the first half of 2022, we’re already seeing these dynamics play out, and gold appears to be doing exactly what investors predict. When other assets aren’t performing well, gold performs well.

Source: Bloomberg, World Gold Council

Impact of the recent geopolitical developments on the US dollar’s role in foreign reserves

The US dollar’s role in international trade is well established, but the world has been gradually evolving toward a more “multicurrency” system, particularly as China’s importance in international trade has grown. Even though gold isn’t an official currency, it plays an important function in the monetary system, especially as a high-quality and liquid component of foreign reserves.

Furthermore, unlike fiat currencies, gold bullion is no one’s liability. While it is rarely utilized as a form of direct exchange, it is frequently an invaluable source of collateral and a hedge against systemic risk events. This helps to explain why central banks have been increasingly interested in gold over the past decade, particularly those from emerging markets, which have historically held a substantial percentage of US dollar assets in their foreign reserves.