Portfolio management amid global monetary tightening and slowing economic growth

Over the past few years, the global economy has seen significant and varied shocks, due to the COVID pandemic and the Russia-Ukraine war. Investors are operating in unknown territory as monetary tightening has recently gained significant steam amid unusually high inflation.

A survey that ran by the World Gold Council and Coalition Greenwich, to comprehend how investors are managing this complex environment, reveal that:

The two main factors influencing allocation decisions are interest rates and liquidity concerns.

Most investors who purchase gold do so to diversify their portfolios and hedge against inflation.

Most gold allocations are strategic and are normally held for more than three years.

Investors remain on edge due to the ebb and flow of high current prices, uncertainty about policy responses, and the threat of a recession. Institutions cite liquidity concerns, portfolio rebalancing, and interest rate projections as equally important factors in short-term portfolio allocation decisions.

Drivers of institutional demand for gold

Interactions with institutional investors show that the major reasons for investing outside of fixed income and equities, are protecting against inflation, reducing portfolio volatility, and diversifying return drivers. Similar findings are drawn from a Mercer poll, which finds that asset owners and managers are revisiting their strategic asset allocations to consider the resilience of their portfolios against increased inflationary pressures, volatility, and potential interruptions to economic growth.

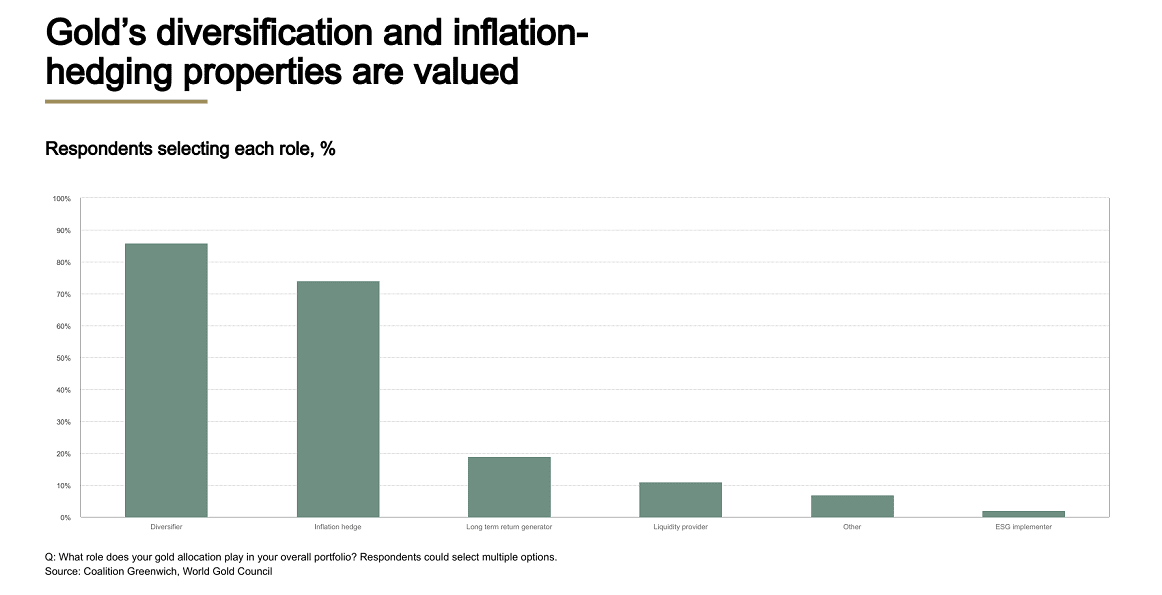

The vast majority of investors who own gold rated diversification and inflation-hedging above all other factors when they were asked to name the primary role that gold plays in their portfolios.

With only around 15% of institutions having explicit gold positions in their portfolios, gold ownership among the investors surveyed continues to be relatively low. Among larger institutions with more than US$10 billion in assets under management (18%) and institutions in EMEA and APAC (18% of respondents in each area), allocations are most common.

The average allocation to gold is a relatively healthy 4%, despite modest general participation by institutional investors. Only a very tiny percentage of investors who have gold allocations expect to lower their allocation over the next three years, the vast majority aim to either retain or increase their present allocation to gold. Additionally, more than half of investors who own gold anticipate retaining it for at least three years, underscoring gold’s importance in their long-term asset allocation strategy.

Institutional allocations to gold will continue to be important, as investors position their portfolios amid this extremely challenging economic environment. These significant allocations to gold reflect institutions’ growing concerns about inflation and their increasing need for efficient portfolio diversifiers during a period of considerable market instability, both in the short and long term.

Moreover, geopolitical risks remain with the ongoing Russia-Ukraine war, and the rising tensions between the US and China. Institutional demand for gold should remain strong going forward due to the requirement for some downside protection in this difficult environment.