What makes gold a strategic asset?

There are diverse sources of demand for Gold, including as an investment, a reserve asset, jewellery, and a technology component. It’s highly liquid, no one’s liability, there’s no credit risk, and it’s rare, thus its value has historically held up.

Gold does not immediately conform to the majority of the most commonly used equities or bond valuation methodology. Typical models based on anticipated cash flows, expected earnings, or book-to-value ratios struggle to provide an appropriate assessment for gold’s underlying value in the absence of a coupon or dividend.

Gold can boost a portfolio in four key ways:

Returns

Diversification

Liquidity

Portfolio Performance

A Source of Returns

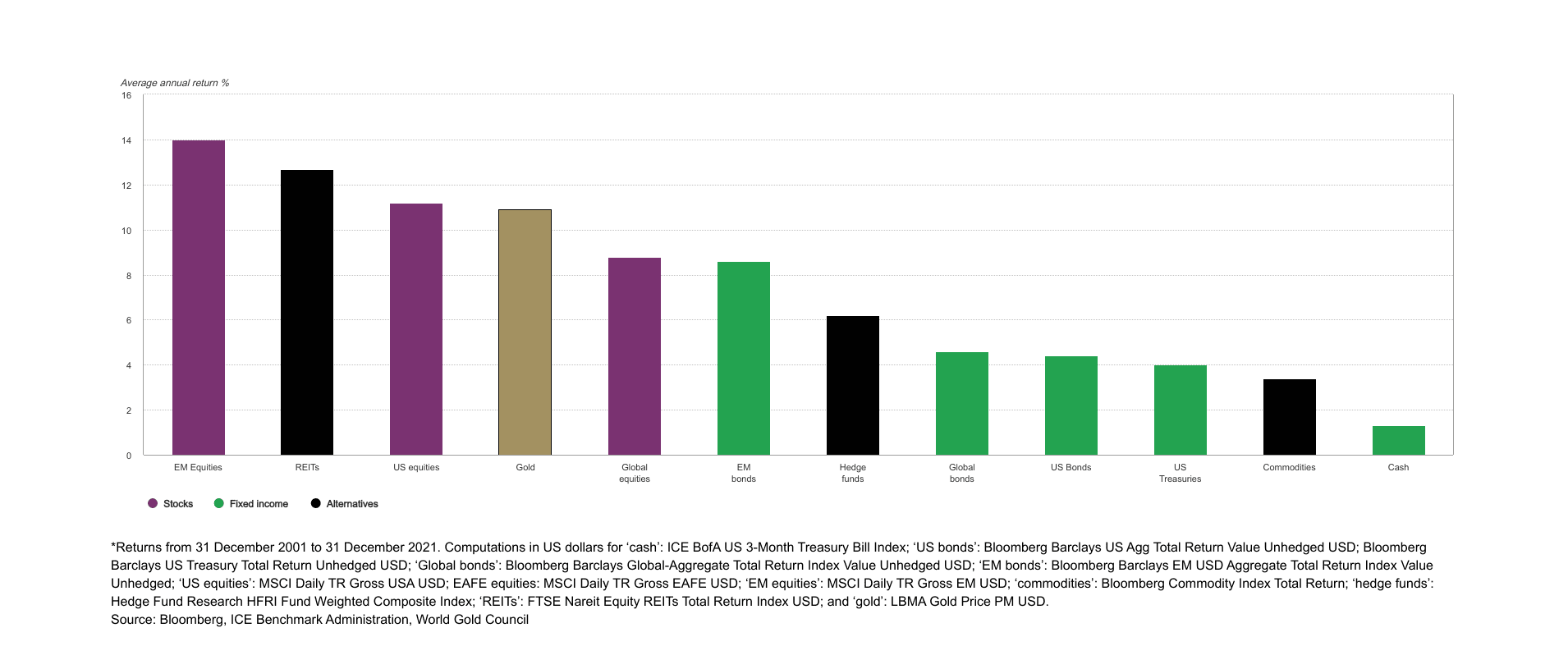

Gold has always been seen as a valuable asset in times of uncertainty by investors. It has historically generated positive long-term returns in both good and poor economic periods. In the nearly half-century after the gold standard collapsed in 1971, the price of gold in US dollars has increased by an average of nearly 11% every year. Gold’s long-term return is equivalent to equities and higher than bonds throughout this time period. Over the past five, ten, and twenty years, gold has outperformed several other key asset classes.

This duality reflects gold’s diverse sources of demand and differentiates it from other investment assets. Due to its global renown, gold is frequently used to protect and enhance wealth through time as it is not a liability, and it can be used as a means of exchange.

Diversification

Diversifiers that work can be difficult to find, sometimes. As market uncertainty grows and volatility increases, many assets become more correlated, driven in part to risk-on/risk-off investing decisions. As a result, many “diversifiers” fail to protect portfolios when they are most needed by investors.

Gold differs from other risk assets in that its negative correlation to equities and other risk assets increases as these assets fall in value. Equities and other risk assets, as well as hedge funds, real estate, and most commodities, which were formerly considered portfolio diversifiers, all tumbled in value. Gold, on the other hand, kept its ground and grew in value, rising 21% in US dollars between December 2007 and February 2009. Gold’s performance remained favourable even during the most recent dramatic equity market pullbacks in 2018 and 2020.

This strong performance is not surprising. Gold has been particularly beneficial during times of systemic risk, providing positive returns and decreasing overall portfolio losses, with few exceptions. Gold also assists investors to meet liabilities when less liquid assets in their portfolio are difficult to sell or are mispriced.

Liquidity

Physical gold holdings by investors and central banks are estimated to be worth US$4.9 trillion, with an additional US$1.2 trillion in open interest in derivatives traded on exchanges or in the over-the-counter (OTC) market, based on the World Gold Council’s estimation.

Gold is also more liquid than several major financial markets, such as the euro/yen and the Dow Jones Industrial Average, while trading volumes are like those of US 1 to 3 years treasuries and US T-Bills. In 2021, gold trade volumes averaged around US$131 billion per day. During that time, OTC spot and derivatives transactions totalled US$72 billion, while gold futures traded $56.3 billion per day across various global exchanges. With global gold ETFs trading an average of US$2.4 billion per day, gold-backed ETFs (gold ETFs) provide an added source of liquidity.

Portfolio Performance

Overall portfolio performance is aided by long-term returns, liquidity, and adequate diversification. When taken together, they suggest that adding gold to a portfolio can significantly improve risk-adjusted returns.

Analysis of investment performance over the past 2, 5, 10 and 20 years, highlights Gold’s positive influence on an institutional portfolio. It indicates that if 2.5%, 5%, or 10% of a US portfolio were allocated to gold, would have resulted in higher risk-adjusted returns and lower drawdowns. This good positive impact has been especially noticeable since the global financial crisis (GFC).

A more comprehensive optimisation analysis based on re-sampled efficiency, in addition to standard back-testing, reveals that an allocation to gold may result in a considerable improvement in portfolio performance. Gold allocations of 6% to 10% in well-diversified US dollar-based portfolios with varied levels of risk, for example, could result in higher risk-adjusted returns.

Inflation, supply-chain concerns and COVID uncertainty

Inflation was a major global theme in 2021, and it will continue to influence investor decisions in 2022. While many central banks (CBs) believed the increase in inflation levels due to COVID’s impact was only temporary in the first half of 2021, this consensus altered in the second half of the year. Some central banks are now recognizing that inflation is here to stay and are planning to boost rates in 2022. Other countries, like China, India, and the European Central Bank, are expected to continue accommodative policies.

Meanwhile, pandemic-related supply chain bottlenecks have not completely dispersed. It is true that governments have been hesitant to respond to the recent spike in COVID cases with formal shutdown measures similar to those that disrupted economic growth in the previous two years, but new variants could change this behaviour, and a resurgence of supply chain disruption – across multiple sectors from technology to shipping – could harm economic growth and add to inflationary pressure.

While the market anticipates rate hikes and a stronger US dollar, both of which are negatives for gold prices, real and nominal rates are expected to remain at historically low levels.

Conclusion

Over the last two decades, perceptions of gold have shifted dramatically, reflecting increased wealth in the East and a growing global recognition of gold’s importance in institutional investment portfolios.

Gold’s unique characteristics as a scarce, highly liquid, and uncorrelated asset show that it can be used as a long-term diversifier. Gold’s position as an investment and a luxury good has allowed it to generate average returns of 11% over the last 50 years, which is comparable to equities but higher than bonds and commodities.

Gold’s traditional function as a safe-haven asset means it shines in high-risk situations. However, because gold is both an investment and a consumer commodity, it may yield positive returns in both good and bad times. This trend is likely to persist, reflecting ongoing political and economic instability, low interest rates, and economic concerns about equity and bond markets.

According to analysis from WGC, adding between 4% and 15% of gold to average hypothetical portfolios, depending on the composition and area, can improve performance and boost risk-adjusted returns on a long-term basis.